Should You Teach Kids to Budget – and When Do You Start?

What Is Budgeting and Why Does It Matter: The Basics for Beginners

A budget is a plan that tells your money where to go before you spend it. That single sentence contains everything a child – or an adult – needs to understand before building any financial habit.

At its core, budgeting has three moving parts: income (money coming in), expenses (money going out), and savings (money set aside for a goal). A budget doesn't restrict freedom – it creates it. When you know exactly how much you have and where it's going, you stop guessing and start deciding. These budgeting basics apply whether you're managing a household of four or handing a 7-year-old their first dollar.

For families learning these concepts together, the Bromoney budget planner app offers a simple starting point – one that works for parents and kids exploring money management side by side.

Why It Matters: What Happens When Kids Don't Learn to Budget

Financial Habits Form in Childhood – Here's What the Research Says

The question isn't whether to teach children about money. The research settled that debate years ago.

A 2016 CFPB report, Building Blocks to Help Youth Achieve Financial Capability, synthesized years of developmental data and concluded that the foundations of financial behavior – self-control, planning, and delayed gratification – are established in childhood and directly predict financial well-being in adulthood. This isn't a theory. It's a measurable pattern.

The University of Michigan found that children as young as 5 already show distinct emotional tendencies around spending versus saving – and those tendencies predict real financial behavior later in life. Money attitudes aren't a math problem. They're a self-regulation problem that starts before kindergarten.

The OECD's PISA 2018 Results (Volume IV): Are Students Smart about Money? (OECD Publishing, 2020) added another layer: teenagers who had practical experience with money – like having a savings account – scored measurably higher on financial literacy assessments than those who didn't. Experience, not just instruction, drives competency.

"Financial education can improve financial knowledge and financial behaviors – and the effect depends on intensity, age, target group, and whether the program is mandatory." – CFPB, A Review of Youth Financial Education: Effects and Evidence

The CFPB review also found that post-2000 state mandates for financial education were associated with higher credit scores, lower default rates, and more deliberate student loan decisions among young adults. That's the downstream impact of financial habits built years earlier.

What Happens Without Financial Education

Children who grow up without money conversations tend to treat spending as automatic and saving as optional. By the time they're 18, the habits are already set.

Data from 2025 confirms it: 82% of adults say they wish they had received financial education earlier in life. A NAFI analytical report from the same year found that only 15% of teenagers without personal budgeting experience could correctly assess the long-term consequences of taking out a loan. That's not a knowledge gap – it's a preparation gap.

In my work reviewing financial intake flows and lending patterns at Bromoney, I see the adult version of this every day. Borrowers who struggle most with debt aren't unintelligent. They simply never learned to connect a decision today with a consequence next month. That skill is built at age 8, not 28.

Should You Teach Kids to Budget? Arguments and the Answer

The Core Arguments for Starting Early

The case is straightforward:

- Habits form early. Cambridge University research suggests that core money habits are established by age 7. By the time a child reaches middle school, patterns of spending and saving are already deeply ingrained.

- Children with early budgeting experience carry stronger credit outcomes. Kids who began tracking personal finances before age 10 tend to carry credit scores averaging 45 points higher as adults.

- Financial literacy reduces anxiety. A 2024 Institute for Financial Wellbeing study found that financial education in childhood lowers financial stress levels in adulthood – not the reverse.

These aren't soft benefits. They're measurable differences between people who learned to use a budget early and those who didn't.

Common Objections From Parents – and Why They Don't Hold Up

"They're too young." This is the most common one. But developmental psychology disagrees. The relevant skills at ages 3-5 aren't compound interest – they're trade-offs, delayed rewards, and the concept that things have prices. Those are exactly what young children can grasp.

"They won't understand." The key is matching the method to the age. A 4-year-old playing "store" with real coins understands more than parents expect. Abstraction fails. Tangible practice works.

"It will ruin their childhood – they'll grow up materialistic." Teaching a child that money is finite and requires choices doesn't produce greed. It produces judgment. The absence of money education – not its presence – creates the adult who overspends, under-saves, and borrows impulsively. As Ron Lieber argues in The Opposite of Spoiled, financial transparency raises children with stronger values, not weaker ones.

At What Age Should You Start Teaching Kids to Budget: A Breakdown by Age

Ages 3-5: First Concepts of Money and Value

At this stage, children learn that money is a medium of exchange – that things have prices and that buying one thing means not buying another. That trade-off is the seed of every budget ever made.

Practical goals: recognize coins and bills, understand that items cost money, and accept that you can't always have everything at once. CFPB's Money as You Grow program recommends tying money conversations to everyday moments – at the store, at the register, at home – rather than treating them as formal lessons. The CFPB is explicit that these conversations are never "too early" and that the developmental window from ages 3 to 7 is particularly important for setting behavioral patterns.

Ages 6-9: A Personal Budget and the First Piggy Bank

This is when regular allowance becomes a teaching tool. Children at this stage connect effort to reward, set a short-term savings goal (a toy, a game), and make deliberate choices about how to spend a small amount.

The University of Wisconsin Extension recommends introducing the "spend-save-share" framework here – dividing money into three categories so that budgeting feels concrete and visual, not abstract. A common rule of thumb used in financial education: $1 per week for each year of age – so a 7-year-old receives $7 weekly. This scales naturally with the child's growing capacity to manage more complex decisions.

Ages 10-13: Expense Planning and Savings Goals

By 10, children handle a real budget with categories. They understand the difference between wants and needs, compare prices, and plan toward a medium-term goal – say, saving for three months to buy something specific.

This is also the right age to introduce the logic of how money accumulates or depletes over time. A debt payoff calculator – even used hypothetically – makes abstract planning feel real. Seeing numbers move in a simple tool is more effective than any lecture about future consequences.

Ages 14-17: Budget as a System – Income, Expenses, Savings

Teenagers handle the full architecture of a personal budget. Income (allowance, part-time job, stipend), fixed expenses, variable expenses, savings rate, and financial goals all fit together into a system they manage independently.

FDIC's Money Smart for Young People curriculum explicitly introduces teen banking, debit cards, savings goals, and introductory credit concepts at this stage – because the goal is to make young adults comfortable with real financial tools before they face them alone. Teen budgeting works best when it's anchored to real accounts and real consequences, not simulations.

How to Teach Kids to Budget in Practice: Methods for Every Age

Games and Visualization for Young Children

For children under 6, the best teacher is play. Here are six methods that work:

- "Store" Game – Assign price tags to household toys, use play money. Goal: understand the exchange process and the concept of price.

- Coin Sorting – Sort real coins by denomination into labeled containers. Goal: recognize money by value, build numeracy through touch.

- Dream Jar – A clear jar with a picture of the desired item taped to it. Goal: make saving visible and goal-oriented.

- "Little Helper" Method – Small tasks (tidying toys) earn a small reward. Goal: connect effort to income.

- "What Do You Need More?" Card Game – Cards showing food, clothing, and toys. Goal: introduce the needs vs. wants distinction.

- Money Workshop – Draw and color your own coins and bills. Goal: learn what money looks like through creative engagement.

The CFPB's Money as You Grow resources reinforce this approach – concrete, physical, and embedded in daily life rather than scheduled as a lesson.

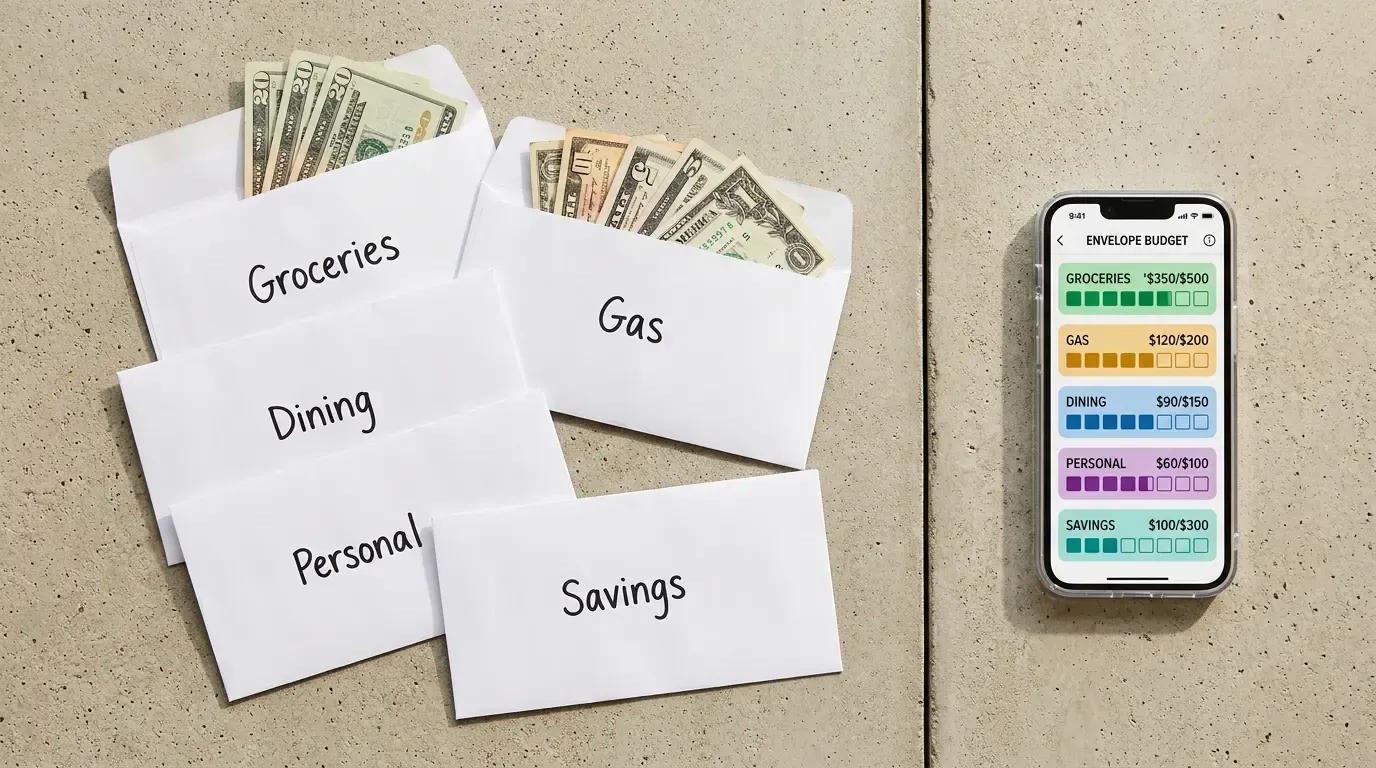

The Envelope System and Allowance for School-Age Kids

The envelope method divides money into physical or visual categories – typically "Spend," "Save," and "Give." For ages 6-9, use transparent jars with picture labels. For ages 10-13, the same logic moves to budgeting apps for families with virtual envelope features.

The method works because it makes limits tangible. A child who can see the "entertainment" jar emptying learns impulse control faster than one who hears an abstract explanation. When the jar is empty, it's empty – and that consequence teaches more than any lecture.

A practical example: a child receives $10 for the week. $4 goes into the "save" jar toward a specific goal, $3 into "spend," and $3 into "give." The rule is simple – you only spend from the right jar. This is the foundation of personal spending allowance management.

Apps and Spreadsheets for Teenagers

Teenagers respond better to digital tools than to physical jars. Apps like Greenlight, FamZoo, and Copper translate the envelope method into a mobile interface that fits how teens already manage their lives. These are the best budgeting apps for teens because they combine real debit card functionality with parental visibility – a combination that physical jars can't replicate.

For families deciding between app-based and spreadsheet-based approaches before committing, the comparison at budgeting apps for families covers the tradeoffs in detail. The Bromoney app also supports goal-based savings tracking, which works well for teenagers building their first real budget alongside a parent account.

Should You Discuss the Family Budget With Your Child – and How?

Yes – with age-appropriate boundaries.

Start at ages 5-7 with basics: the family has income, the family has expenses, and some things cost more than others. By ages 11-14, share the structure of the household budget in percentages (housing, food, savings, leisure) and involve them in planning shared expenses like a vacation.

What to avoid: specific salary figures that create anxiety, or detailed debt discussions that transfer adult stress to a child. The goal is to teach principles, not to burden them with problems they can't solve.

Research from Cambridge University shows that children who grow up with open family money conversations are more likely to maintain personal budgets, use savings deliberately, avoid impulsive borrowing, and report lower financial anxiety as adults. For households managing joint expense tracking, bringing older children into those conversations – even partially – accelerates their financial development.

Common Parenting Mistakes When Teaching Kids About Money

"Money Is Not for Kids" – and Other Beliefs That Backfire

Phrases like "money is not for children" or "we don't talk about finances" create a silence that costs more than any bad purchase. Children who don't receive answers to money questions grow up without vocabulary, without frameworks, and without the capacity to make deliberate financial decisions.

The theory of social learning explains why: children absorb financial behavior by watching adults. A parent who never discusses money – or who panics visibly about it – teaches a lesson regardless. The question is only whether that lesson is intentional.

CFPB guidance consistently supports calm, routine money talk rather than emotional secrecy. Money doesn't need to be a special occasion topic. It fits naturally into grocery trips, utility bills, and vacation planning – any moment where a family makes a choice under constraint.

The "Give Everything Without Explanation" Mistake

When a child receives money on demand, without structure or discussion, they absorb one message: money appears when needed and disappears without consequence. That model produces adults who overspend, under-save, and reach for credit when the jar runs empty.

Ron Lieber's The Opposite of Spoiled identifies three specific patterns that undermine financial education: rescue behavior (covering every overspend), using money as punishment or reward for unrelated behavior, and inconsistency in allowance rules. All three signal to the child that money follows emotion, not planning.

The better model: a consistent allowance, clear budget categories, and – critically – no rescue when the money runs out before the week does. Low-stakes consequences are the most effective teacher in personal finance. CFPB guidance explicitly recommends letting children experience the result of their choices rather than correcting every mistake immediately.

Frequently Asked Questions

At What Age Should You Give a Child an Allowance?

The research-backed answer is 6-7 years old. At this age, children understand basic math, recognize the value of different denominations, and connect saving with a concrete goal. Starting earlier is possible for basic concepts; starting later means missing the formative window for habit development.

A common rule of thumb used in financial education circles: $1 per week for each year of age – so a 7-year-old receives $7 weekly. This is an approximation, not a universal law, but it scales naturally with the child's growing capacity to manage more complex decisions.

Should You Tell Kids About the Family Budget?

Yes – in age-appropriate terms. Children don't need exact salary figures. They need to understand that income is finite, that it covers essential expenses first, and that families make trade-offs. CFPB's parent resources support short, calm explanations of priorities without transferring adult financial stress.

What Do You Do When a Child Spends Everything at Once?

Three strategies work consistently:

- Three-jar method – Divide money into "Spend," "Save," and "Give" before any purchasing decision. The structure prevents impulsive allocation.

- Goal anchoring – Help the child identify a specific purchase they want, calculate how many weeks of saving it requires, and track progress visually.

- No rescue – If the money is gone before the week ends, don't replenish it early. The discomfort of an empty jar teaches planning faster than any conversation. The University of Michigan research on childhood spending tendencies confirms that children who are naturally spend-oriented benefit most from structural constraints – not lectures.

What Apps Help a Child Track Their Budget?

For U.S. families, Greenlight is the most widely used – over 7 million families as of 2026. FamZoo offers more flexibility for older teens, including a family-bank model with internal loans. Copper and Current target 13+ users with a teen banking focus. See the full comparison table in the apps section below.

The Benefits of Budgeting: From Savings to Financial Freedom

The numbers behind budgeting are consistent across recent research:

- 65% of people who budget regularly report lower financial stress, compared to 30% among those who don't (Financial Health Network, 2024)

- Households with a budget save an average of 15% more income and are twice as likely to maintain a 3-month emergency fund (Bank of America, 2025)

- 70% of budgeting app users report feeling greater control over their finances

- People who start budgeting before age 30 are 40% more likely to reach financial independence by age 55 (McKinsey, 2025)

These aren't aspirational outcomes. They're measured differences between people who plan and people who don't. A budget helps not by restricting choices but by making them visible – and visible choices are the ones people actually control.

How to Build Your First Budget: A Step-by-Step Guide

Step 1: Assess Your Income

Add up every dollar coming in during the month – allowance, part-time job earnings, stipend, cash gifts. This total is your starting number. Everything else is built around it. For a teenager creating their first budget, this step alone is clarifying: most people genuinely don't know how much they earn until they write it down.

Step 2: Track Your Expenses

Spend one full month recording every transaction. Use a notes app, a spreadsheet, or a dedicated budgeting tool. The goal is a complete, honest picture of where money actually goes – not where you think it goes. Most people are surprised by the gap.

Step 3: Create Budget Categories

Group your recorded expenses into categories: Transportation, Food, Entertainment, Subscriptions, Savings. For a first budget, the 50/30/20 rule – popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in All Your Worth (2005) – provides a clean starting framework: 50% to needs, 30% to wants, 20% to savings and debt. Adjust the ratios to fit your actual life.

For a deeper look at how to structure budget categories across a household, the joint expense tracking guide covers shared-budget architecture in detail.

Step 4: Set Savings Goals

A budget without goals is just a ledger. Define specific, time-bound targets: "Save $400 for a new phone in 8 weeks" is a goal. "Save more money" is not. Assign each savings goal its own budget line and treat it like a fixed expense – not what's left over.

Step 5: Review and Adjust Monthly

At month's end, compare plan to reality. Where did you overspend? Where did you underspend? Adjust the next month's plan accordingly. A budget that never changes isn't a budget – it's a wish list. Smart financial notification management flags when spending approaches category limits before the damage is done.

Budgeting for Young People: Advice for Teens and College Students

For Teenagers

Financial educators consistently recommend one starting rule for teen budgeting: pay yourself first. The moment any income arrives – allowance, job paycheck, birthday cash – transfer 10-20% to a separate savings account before spending anything else. This single habit, automated and consistent, produces more long-term financial stability than any other single behavior.

Research supports the specifics: teenagers who earn their own money are 40% more likely to develop consistent saving habits than those who receive only allowance. The act of earning changes the relationship to spending.

For impulse control, apply the 30-day rule: if you still want a non-essential item after 30 days, the purchase is likely justified. Most impulse wants evaporate within a week.

For College Students

Budgeting for college students follows the same architecture as any personal budget – but the constraints are tighter and the stakes are higher. The 50/30/20 framework adapts naturally to student life: 50% of income covers fixed necessities (rent, food, transportation), 30% covers discretionary spending (social activities, subscriptions, hobbies), and 20% goes directly to savings or debt repayment.

Budgeting for young adults in college also means separating one-time costs from monthly obligations. A semester's worth of textbooks hits differently than a $15/month streaming subscription – but both need a line in the budget. For students managing tracking family subscriptions alongside their own recurring expenses, that separation is the first step toward a budget that actually reflects real spending patterns.

Best Budgeting Apps for Teenagers: A Comparison

| App | Key Features | Target Age | Pros | Cons | Cost |

|---|---|---|---|---|---|

| Greenlight | Debit card, parental controls, spend/save/give categories, investment option | 6-18 | Most balanced feature set; 7M+ families; real debit card | No free tier | From $5.99/mo |

| GoHenry | Debit card, gamified "money missions," financial literacy modules | 6-18 | Strong educational content; engaging for younger kids | Per-child pricing adds up for larger families | ~$5-10/mo per child |

| FamZoo | Family bank model, internal loans, parent-managed accounts, interest simulation | 4-17 | Most flexible; great for older teens; teaches real banking logic | Steeper learning curve for parents | ~$5.99/mo (family) |

| Copper | Teen checking account, P2P transfers, spending insights | 13+ | Free basic account; feels like real banking | Limited parental oversight features | Free (basic) |

| Current | Teen debit card, savings pods, instant notifications | 13+ | Clean UX; strong for independent teens | Less educational structure | Free (basic) |

| RoosterMoney | Virtual account (no card required), goal tracking, chore management | 4-17 | Can start without a card; good for younger children | Card access requires paid plan | Free (virtual); paid for card |

Note: All listed apps are designed for the U.S. or U.K. market and require linking to domestic banking systems. Availability outside these regions is limited as of 2026.

How to Teach Children to Manage Money: Methods and Worksheets

Below are quiz questions by age group. Use them as a family conversation starter or a quick check-in after introducing a new concept. These teaching budgeting worksheets in question format work because they surface gaps in understanding without making the child feel tested.

Ages 6-9

- What is "income"? → All money you receive: allowance, gifts from family.

- Why do we save money? → To buy something big that we can't afford right now, like a bike.

- You have $1.00. Can you buy a $0.60 juice and a $0.50 chocolate bar? → No – you have to choose one.

Ages 10-13

- What is a personal budget? → A plan for your income and expenses that shows where your money goes each month.

- What's the difference between income and expenses? → Income is money coming in; expenses are money going out.

- You want a $100 item and earn $10 per week. How long do you save if you set aside $5 each week? → 20 weeks.

Ages 14-17

- Why should income always exceed expenses? → To build savings for goals and emergencies, and to avoid debt.

- What is a bank savings account? → A tool that holds your money and pays you interest over time.

- Why set financial goals? → To give saving a purpose and create motivation to control spending.

Budgeting for a Child: How to Plan Expenses for Your First and Second Baby

Core Expense Categories

Raising a child in the U.S. involves costs that compound across years. The primary categories:

- Food and nutrition (30-40% of child-related spending)

- Clothing and footwear (15-20%)

- Healthcare and hygiene (10-15%)

- Education and enrichment (highly variable – the largest wildcard)

- Childcare (often the single largest line item for families with young children)

For families building this budget from scratch, the how to build a family budget guide covers the full household architecture, including how to integrate child-related costs without destabilizing other financial goals.

How Expenses Change With a Second Child

A second child doesn't double costs – but it comes close. Research from 2024-2026 data shows that total child-related expenses increase by 60-80% with a second child, not 100%, because many items (clothing, stroller, books, toys) are reused.

Budgeting tips for a second child start with identifying what carries over and what doesn't. Clothing and gear reuse cuts costs significantly. The new pressure points are housing (larger space), simultaneous childcare for two, and the compounding cost of two sets of educational and extracurricular activities. Families planning for a second child benefit from a budget review 12 months before the expected arrival – not after.

For context: in South Korea, private education costs per child rank among the highest globally. In Germany, state subsidies significantly reduce the childcare burden. In the U.S., the absence of universal subsidized childcare means families absorb the full market rate, which averaged $1,230-$2,400/month per child for center-based care in 2025, depending on region. Budgeting for a second child in the U.S. requires accounting for that full rate across two children simultaneously – a figure that reshapes the entire household budget.

Budgeting Tools and Systems: Find the Method That Works for You

Method 1: 50/30/20 Popularized by Senator Elizabeth Warren and Amelia Warren Tyagi in All Your Worth (2005). Divide after-tax income: 50% to needs, 30% to wants, 20% to savings and debt. Best for beginners who want a simple budgeting strategy without detailed tracking. Limitation: the needs/wants boundary is blurry, and the 50% ceiling doesn't work in high cost-of-living cities.

Method 2: Envelope Method Divide cash (or digital equivalents) into labeled categories. Spend only from the correct envelope. Best for people who overspend impulsively or need visual reinforcement. This budgeting system is particularly effective for school-age children because the physical constraint is immediate and undeniable. Limitation: friction with digital and online payments.

Method 3: Zero-Based Budgeting Every dollar of income is assigned a job. Income minus all allocations equals zero. Best for people with variable income or those who want maximum visibility into their finances. Limitation: time-intensive – requires rebuilding the budget each month from scratch.

Method 4: Pay Yourself First Immediately after income arrives, transfer a fixed amount to savings or investment. Spend the remainder. This budgeting method is the foundation of the "pay yourself first" habit that financial educators recommend starting in the teen years. Best for anyone who wants to guarantee savings without tracking every expense. Limitation: doesn't address overspending in daily categories, which leads to debt if the remainder isn't enough.

For families deciding between a structured app and a manual spreadsheet approach, the budgeting apps for families comparison breaks down which tool fits which budgeting method best.

Conclusion: When to Start – There Is No "Too Early"

The research consensus in 2026 is clear: the best time to teach a child about money was yesterday. The second-best time is now.

"Teaching budgeting in preschool isn't about numbers – it's about building self-control and delayed gratification. A child who learns to divide allowance into 'want now' and 'saving for a dream' gets a foundational skill for future emotional and financial stability." – Anna Morozova, child psychologist, Children and Money (2024)

"The budgeting skill established before age 10 reduces the risk of impulsive debt in adult life by 40%. It's not just about counting – it's a vaccine against financial stress." – Pavel Sidorov, financial consultant, Forbes interview (2023)

The CFPB is explicit: it is never too early to start, and it is never too late. A 5-year-old playing store with real coins is building the same neural pathways that will later determine whether they comparison-shop a mortgage or sign the first offer they see.

Start with what your child can grasp today. Add complexity as they grow. Be consistent, be calm, and let the consequences of small decisions teach what no lecture can.

"Only 15% of teenagers without personal budgeting experience could correctly assess the long-term consequences of a loan. This skill is the key to reducing over-indebtedness in the next generation." – NAFI Analytical Report, 2025

The families I see at Bromoney who navigate financial difficulty most successfully share one trait: they grew up in homes where money was discussed openly, mistakes were allowed to sting a little, and saving had a visible purpose. That environment doesn't require wealth. It requires intention.

Sources referenced in this article:

- CFPB – Money as You Grow: consumerfinance.gov

- CFPB – A Review of Youth Financial Education: Effects and Evidence: files.consumerfinance.gov

- FDIC – Money Smart for Young People: fdic.gov

- University of Michigan – Children Form Attitudes About Money at a Young Age: michiganross.umich.edu

- OECD – PISA 2018 Results (Volume IV): Are Students Smart about Money?: OECD Publishing, 2020

- University of Wisconsin Extension – Children and Money: Fun Ways to Grow Money Minds: finances.extension.wisc.edu

Denis Goncharenko

Managing Editor & FinTech Content Strategist

Editorial Policy: Denis ensures every financial claim is backed by institutional data sources.

Was this article helpful?

Same blogs

The Envelope Method's Hidden Traps: When Your Budget Creates a False Sense of Financial Security

The envelope method feels like control. But in reviewing household budgets, the same pattern keeps appearing: people who follow their envelopes religiously and still end up in financial crisis. Here's why the envelopes were full while the financial picture was not.

How to Allocate Budget Categories for a Family Making $40,000–$60,000 a Year

A family earning $40,000–$60,000 a year sits well below the $83,730 U.S. median household income – but a structured budget makes financial stability achievable. This guide breaks down every major spending category by percentage and dollar amount, with sample monthly templates for three income levels and a prioritized savings and debt-payoff sequence built for 2026 tax parameters.

Digital Envelope Apps vs. Physical Cash Envelopes: Which Budgeting System Is Right for You?

About 15% of active budgeters use the envelope method – 11% go digital, only 4% stick with cash. This guide breaks down exactly how each system works, where each one fails, and how to pick the one that fits how you actually spend money.