How to Build a Family Budget You'll Actually Stick To (Without Feeling Deprived)

What Is Budgeting and Why It Matters for Your Family's Financial Health

Budgeting is the practice of intentionally directing every dollar of your income toward specific categories – housing, groceries, savings, debt – before that money has a chance to disappear into the void of daily spending. For a family, it's not just accounting. It's a shared decision about what matters most.

The numbers back this up. A 2024 study published in the Journal of Financial Economics found that households with an active budget reduced their non-mortgage debt by an average of 15% over two years. According to the Federal Reserve's 2024 Report on the Economic Well-Being of U.S. Households, families who budget consistently are 40% more likely to maintain savings that cover three to six months of expenses. Stanford University research from 2023 showed that the act of planning itself – regardless of the tool used – reduces financial stress by 25%, simply because it restores a sense of control.

Yet most American families struggle not with the concept but with execution. An annual survey by Debt.com found that more than 8 in 10 Americans say they have a budget – but NerdWallet's 2023 report found that 83% of Americans overspend at least sometimes, with nearly half (47%) citing food as the primary culprit. The gap between planning and doing is where most budgets collapse.

This guide closes that gap.

"In its annual budgeting survey, Debt.com reveals that more than 8 in 10 Americans budget – a 16% increase over the last five years." – Debt.com Budgeting Survey, 2025

How to Build a Family Budget in 7 Steps (Quick Overview)

Here's the full process at a glance. Each step is covered in depth below.

- Add up your total household income – calculate real take-home pay, including side income and benefits

- Track and list every monthly expense – fixed, variable, discretionary, and family-specific

- Choose a budgeting method – 50/30/20, zero-based, envelope, or pay-yourself-first

- Set up budget categories and allocations – with sinking funds and built-in fun money

- Set meaningful family financial goals – short, mid, and long-term, with your partner aligned

- Choose your budgeting tools – apps, spreadsheets, or hybrid systems

- Stick to the budget without misery – build flexibility, run monthly check-ins, adjust instead of quitting

How to Create a Budget: A Step-by-Step Guide for Beginners

If you've never tracked a dollar in your life, start here. Building a budget for the first time feels overwhelming – until you break it into four concrete actions.

First, gather your numbers. Pull three months of bank statements and credit card statements. Don't guess. Look at what actually happened, not what you think happened. Most people are surprised: the average U.S. household spends $77,280 per year, according to the Bureau of Labor Statistics' 2024 Consumer Expenditure Survey – but few families could name that number off the top of their heads.

Second, separate income from expenses. Write down every dollar coming in (after taxes) and every dollar going out. Put them in two columns. If the second column is larger than the first, that's your starting point – not a reason to panic. Having a budget means knowing exactly where that gap is, which is the only way to close it.

Third, categorize your spending. Group expenses into needs (rent, utilities, groceries), wants (subscriptions, dining out, hobbies), and savings or debt payments. This single act of categorization reveals where money leaks.

Fourth, assign limits going forward. Based on your categories and income, set a monthly spending limit for each bucket. This is your first budget. It won't be perfect. That's expected. The goal in month one is awareness, not perfection.

For families new to this process – budgeting 101, as it's often called – the 50/30/20 rule (50% needs, 30% wants, 20% savings and debt) works as a starting framework. It's simple enough to implement immediately and flexible enough to adjust as your picture gets clearer. Creating a budget this way takes under two hours the first time.

What Is a Family Budget (And Why Most Families Struggle With One)

Family Budget vs. Personal Budget: Key Differences

A personal budget answers to one person. A family budget answers to multiple people with different spending habits, different emotional relationships with money, and different definitions of "necessary." That complexity changes everything.

When one partner prioritizes retirement savings and the other prioritizes a family vacation, no spreadsheet resolves that tension automatically. The budget becomes a negotiation tool, not just a math exercise. Family budgeting requires both a system and a shared agreement – not just numbers on a page.

Why Traditional Budgets Fail Real Families

Behavioral economics research from 2024 and 2025 identifies four psychological patterns that derail family budgets:

- Optimism bias – families consistently underestimate the probability of unexpected expenses

- Present bias – the immediate pleasure of a purchase outweighs a distant savings goal

- Decision fatigue – constant spending decisions exhaust mental resources, leading to impulsive choices

- All-or-nothing thinking – one overspent month feels like total failure, triggering complete abandonment

Add to this the structural reality: the Federal Reserve's 2024 SHED report found that 85% of adults said rising prices affected their family budget at least somewhat. A budget built in January becomes outdated by April if it isn't reviewed regularly.

The Real Goal: A Spending Plan That Works for Your Whole Family

Reframe the word "budget." It's not a restriction. It's a spending plan – a document that says: here's what we earn, here's what we value, and here's how we make those two things match. Families that approach it this way stick with it longer, argue about money less, and reach their goals faster. Plan a budget once and you'll spend the rest of the year adjusting it. That's not failure – that's how it works.

Step 1 – Add Up Your Total Household Income

How to Calculate Your True Take-Home Pay

Take-home pay is not your salary. It's what lands in your bank account after federal and state taxes, Social Security, Medicare, and any pre-tax deductions (401(k) contributions, health insurance premiums) are removed.

Use this formula:

Gross Income → minus pre-tax deductions → minus taxes = Net Take-Home Pay

For budgeting purposes, always work from net income. Building a budget around your gross salary is one of the most common first-time mistakes I see – and it creates a shortfall before you've spent a single dollar.

What to Do If Your Income Is Variable or Irregular

If your household income fluctuates – freelance work, commission-based pay, seasonal employment – use a conservative baseline. Calculate your average monthly net income over the last 12 months, then budget from the lowest three-month average, not the highest.

The CFPB and NFCC both recommend building a stabilization fund equal to one to three months of baseline expenses before anything else. This buffer absorbs the low-income months without forcing you into debt.

A practical system: two accounts. All income flows into Account A. A fixed monthly transfer goes to Account B (your spending account) to cover planned expenses. Anything extra in Account A becomes savings or accelerated debt payoff.

Including All Income Sources (Side Hustles, Benefits, Child Support)

Your full income picture includes:

- Primary employment (net pay after deductions)

- Side hustle or freelance income (average monthly, after self-employment tax)

- Government benefits (SNAP, EITC, Child Tax Credit – these are real dollars)

- Child support or alimony received

- Rental income, dividends, or any other recurring inflows

Document all of it. Families that ignore tax credits and benefit income undercount their resources and build unnecessarily tight budgets. The Federal Reserve's SHED data consistently shows that tax credits like the EITC and Child Tax Credit represent a meaningful portion of net income for low- and middle-income households – leaving them out of your income calculation distorts the entire plan.

"Confronted with higher living costs, 72% of young adults took action to improve their financial health – including seeking additional work, changing jobs, or requesting a raise." – Bank of America Better Money Habits Study, 2025

Step 2 – Track and List Every Monthly Expense

Fixed Expenses: What They Are and What to Include

Fixed expenses don't change month to month. They're non-negotiable obligations:

- Mortgage or rent

- Car payment(s)

- Insurance premiums (health, auto, home/renters, life)

- Minimum debt payments (student loans, credit cards)

- Subscriptions with annual or monthly fixed billing

List these first. They form the floor of your budget – the number you must cover before anything else.

Variable Expenses: Groceries, Gas, and the Unpredictable Ones

Variable expenses fluctuate but are still predictable categories:

- Groceries

- Gas and transportation costs

- Utilities (electric, gas, water – these vary seasonally)

- Medical co-pays and prescriptions

- Household supplies

For variable categories, calculate a three-month average from your statements and use that as your monthly budget target. Don't guess – the average U.S. household spends $9,985 annually on food alone, per BLS 2024 Consumer Expenditure Survey data. That's $832 per month before a single restaurant meal.

Discretionary (Wants) Spending: Where Families Often Go Wrong

Discretionary spending is where budgets get emotional. Dining out, streaming services, hobbies, clothing beyond basics, entertainment – these are the categories that feel essential until you see them totaled.

The key isn't eliminating discretionary spending. It's capping it intentionally. Families that zero out the "wants" category to accelerate savings almost universally quit budgeting within 90 days. The budget needs room to breathe.

Family-Specific Expenses (Childcare, School, Activities)

These categories are invisible in most generic budgeting templates and devastating when forgotten:

- Childcare or daycare

- After-school programs and tutoring

- School supplies, field trips, class fees

- Sports and extracurricular activities

- Summer camps or childcare gaps

The BLS data shows U.S. families spend an average of $2,800 annually on education and childcare – but that figure averages across all household types, including those without young children. For a family with two kids in daycare, this number exceeds $24,000 per year in many metro areas.

Sample Family Expense Categories with Average Costs

| Category | Annual Average (BLS 2024) | Monthly Estimate | % of Total Spending |

|---|---|---|---|

| Housing (mortgage/rent + utilities) | $25,100 | $2,092 | 32% |

| Transportation | $12,650 | $1,054 | 16% |

| Food (groceries + dining out) | $10,200 | $850 | 13% |

| Healthcare | $6,050 | $504 | 8% |

| Utilities (if separate from housing) | $4,900 | $408 | 6% |

| Entertainment & Recreation | $4,100 | $342 | 5% |

| Education & Childcare | $2,800 | $233 | 4% |

| Clothing & Personal Care | $2,100 | $175 | 3% |

| All Other (savings, misc.) | $9,380 | $782 | 12% |

| Total | $77,280 | $6,440 | 100% |

Source: Bureau of Labor Statistics, Consumer Expenditure Survey 2024

Step 3 – Choose a Budgeting Method That Fits Your Family

The 50/30/20 Rule – Simple and Flexible

Split your after-tax income into three buckets: 50% needs, 30% wants, 20% savings and debt repayment.

This is the right starting point for most families new to budgeting. It requires no app, no spreadsheet expertise, and no financial background. The math is fast. The categories are intuitive.

The honest limitation: many families – especially those in high-cost metros or with young children – find that their "needs" already consume 60% or more of income. When that happens, temporarily compress "wants" to 15-20% and treat the gap as a signal to either reduce fixed costs or increase income, not a reason to abandon the framework.

"The 50/30/20 budgeting rule refers to a common way to allocate income – specifically, 50% of income to needs, 30% to wants, and 20% to savings." – Chase Bank, 50/30/20 Budget Rule

For a deeper comparison of 50/30/20 versus zero-based budgeting, see our full breakdown at 30/20 vs Zero Budgeting.

Zero-Based Budgeting – Every Dollar Has a Job

Income minus all assigned expenses, savings, and debt payments equals zero. Every dollar is allocated before the month begins.

This budgeting method surfaces waste fast. When you assign $200 to dining out and $150 to streaming services and $80 to gym memberships, you see the total before you've spent it. That visibility changes behavior.

The tradeoff: zero-based budgeting is time-intensive. It requires monthly setup and regular tracking. For families with irregular income, it's particularly powerful – and particularly demanding. The payoff is total control.

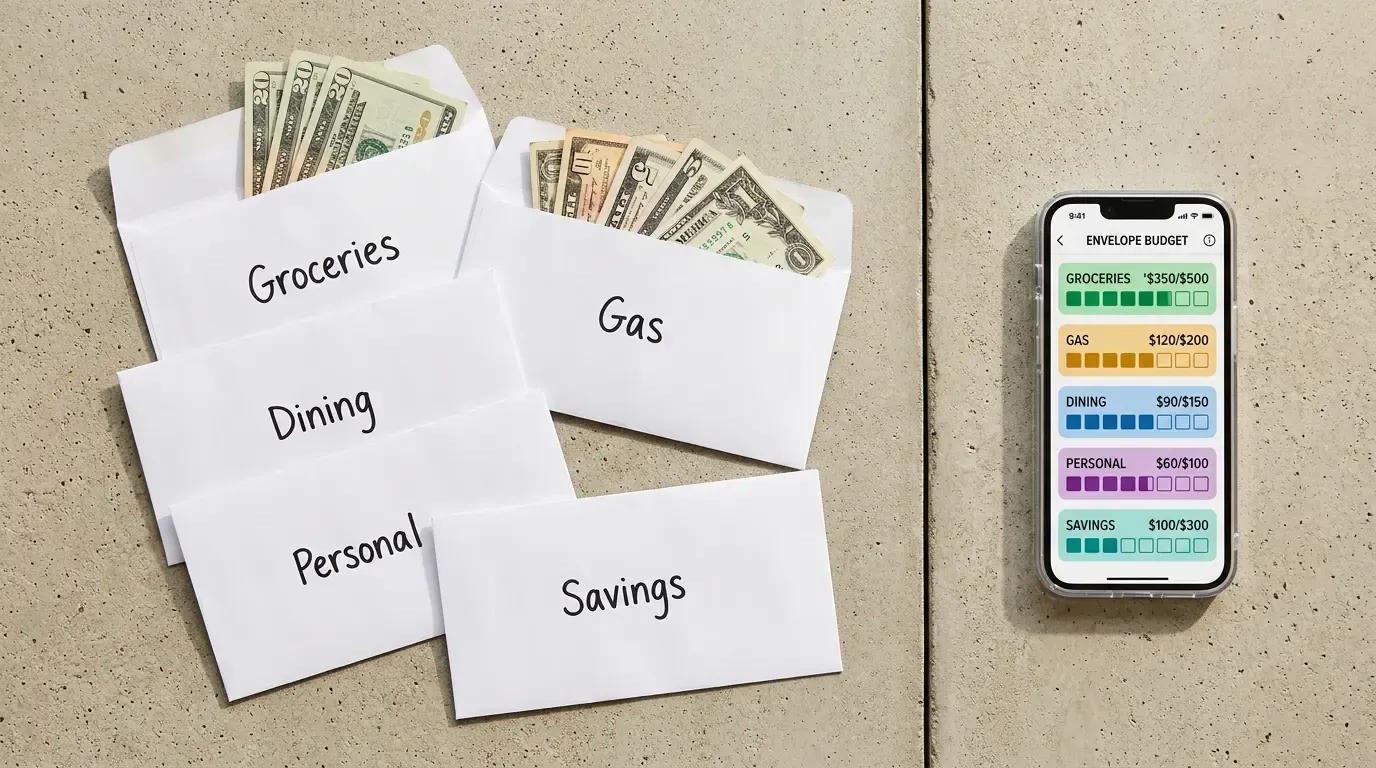

The Envelope Method (Cash and Digital)

Allocate cash into physical envelopes labeled by category – groceries, gas, entertainment. When the envelope is empty, spending in that category stops for the month.

The digital version uses sub-accounts or app-based "envelopes" (YNAB, EveryDollar, and Monarch Money all support this). This adaptation makes envelope budgeting practical for families who rarely use cash.

One key benefit of envelope budgeting: it creates a hard stop on variable overspending. Unlike a credit card that lets you exceed any mental limit, an empty envelope ends the conversation. The system works especially well for categories where overspending is habitual.

Pay Yourself First – Savings-First Approach

On payday, immediately transfer your savings target to a separate account. Budget the remainder for everything else.

This is the budgeting strategy I most often recommend to families who struggle with saving because they spend first and save "whatever's left" – which is usually nothing. Automating the transfer removes willpower from the equation entirely. The CFPB explicitly recommends automatic recurring transfers as one of the most reliable savings behaviors.

Budget Method Comparison for Families

| Method | How It Works | Complexity | Flexibility | Best For | Main Drawback |

|---|---|---|---|---|---|

| 50/30/20 | Split income: 50% needs / 30% wants / 20% savings | Low | Medium | Stable-income families new to budgeting | Doesn't work well when "needs" exceed 50% |

| Zero-Based | Every dollar assigned; income minus expenses = $0 | High | High | Variable income; aggressive debt payoff | Time-intensive; requires monthly setup |

| Envelope Method | Cash (or digital sub-accounts) per category; stop when empty | Medium | Low | Impulse spenders; visual learners | Inconvenient for online/card purchases |

| Pay Yourself First | Save first; spend the rest freely | Low | High | Stable income; already covering basics | May underfund essential categories if savings % is too high |

| 6 Jars / 6 Accounts | Income split across 6 accounts (55% living, 10% fun, 10% savings, 10% education, 10% large purchases, 5% giving) | Medium | Medium | Families seeking holistic financial structure | Fixed percentages may not fit every income level |

Step 4 – Set Up Your Budget Categories and Allocations

Must-Have Family Budget Categories (With Recommended Percentages)

Based on the 50/30/20 framework and BLS data, here are practical allocation targets:

| Category | Recommended % of Net Income |

|---|---|

| Housing (rent/mortgage + utilities) | 25-35% |

| Transportation | 10-15% |

| Groceries | 10-15% |

| Healthcare | 5-10% |

| Childcare / Education | 5-15% (varies widely) |

| Savings (emergency + goals) | 10-20% |

| Debt repayment (above minimums) | 5-15% |

| Entertainment / Discretionary | 5-10% |

| Fun money (individual) | 2-5% |

These aren't rules. They're targets. Your actual numbers depend on your income, location, debt load, and family size. The goal is to make every allocation a conscious choice, not an accident.

How to Build in 'Fun Money' Without Blowing Your Budget

Fun money is a fixed, non-accountable allowance for each adult in the household. It's not a luxury. It's a structural requirement for budget sustainability.

Families that eliminate discretionary personal spending entirely report higher rates of budget abandonment within three months. Fun money – even $30 to $75 per person per month – removes the resentment that kills budgets. Each partner spends their allocation however they choose, no questions asked. This preserves autonomy and prevents the budget from feeling like a prison.

For a full breakdown of why this category matters more than most families realize, read our piece on why fun money is non-negotiable for budget stability.

Sinking Funds: The Secret to Handling Irregular Expenses

A sinking fund is a dedicated savings account for a known future expense. Divide the total cost by the number of months until you need it and save that amount monthly.

Examples:

- Car registration ($300/year) → $25/month

- Holiday gifts ($600/year) → $50/month

- Annual vacation ($1,800) → $150/month

- Home maintenance ($1,200/year) → $100/month

According to NerdWallet's research on holiday spending, 35% of Americans describe their 2025 holiday spending as financially irresponsible – they took on debt or overspent. Sinking funds convert these "surprise" expenses into predictable monthly line items. The surprise disappears. The debt never happens.

Families that build sinking funds for irregular expenses report significantly less financial stress and fewer emergency credit card charges. This approach also connects directly to separating one-time vs. recurring expense categories – a distinction that makes or breaks budget accuracy.

Where to Put Savings in Your Budget (Before Spending)

Savings belong at the top of your budget, not the bottom. Schedule an automatic transfer on payday – before discretionary spending begins.

Target sequence:

- Emergency fund (until you reach 3-6 months of expenses)

- Employer 401(k) match (free money – always capture this first)

- High-interest debt payoff

- Mid-term goals (home down payment, car replacement)

- Long-term goals (retirement, 529 plan)

If you're carrying high-interest credit card debt, use our debt payoff calculator to model how much faster you can eliminate it by directing an extra $100 or $200 per month.

"The key insight from our work with families is that savings must be automated and treated as a non-negotiable expense – not a reward for good behavior at the end of the month. The families who succeed treat their savings transfer like a mortgage payment: it's not optional." – Certified Financial Planner, National Foundation for Credit Counseling (NFCC)

Step 5 – Set Meaningful Family Financial Goals Together

Short-Term Goals (Vacation, Holiday Fund, New Appliance)

Short-term goals have a timeline under 12 months. The math is simple: divide the total cost by the number of months remaining. A $1,200 vacation in 10 months requires $120 per month in a dedicated sinking fund.

Keep short-term goals visible. A shared note, a whiteboard, a savings tracker inside your budgeting app – whatever creates daily awareness. Families that can see progress toward a goal are significantly more motivated to protect the budget categories that fund it.

Mid-Term Goals (Emergency Fund, Debt Payoff, Home Down Payment)

Mid-term goals span one to five years and require sustained discipline:

- Emergency fund: Target three to six months of essential household expenses. For a family spending $4,500/month on basics, that's $13,500 to $27,000. Build this before aggressively investing. The Federal Reserve's SHED 2024 report found that 63% of adults could cover a $400 emergency with cash – but a 2026 U.S. News Financial Wellness Survey found that 43% couldn't cover a $1,000 unexpected expense from savings. The gap between those two numbers is where most families live.

- Debt payoff: Use the avalanche method (highest interest rate first) to minimize total interest paid, or the snowball method (smallest balance first) for psychological momentum. Both work – pick the one you'll actually execute.

- Home down payment: Plan for 10-20% of the purchase price. On a $350,000 home, that's $35,000 to $70,000. At $500/month saved, you reach $35,000 in roughly six years.

Long-Term Goals (Retirement, Kids College Fund / 529 Plan)

Long-term goals require time more than large amounts. Compound interest does the heavy lifting – but only if you start.

- Retirement: Most financial planners recommend saving at least 15% of pre-tax income. If your employer matches 3%, contribute at least enough to capture that match before directing money elsewhere.

- 529 Plan (college savings): To cover a public university education starting from birth, contribute $300-$500 per month. Starting later requires larger monthly contributions. Every year of delay narrows the window significantly.

How to Get Your Spouse or Partner on the Same Page

Financial disagreements are among the leading drivers of marital conflict. A Debt.com survey on debt and divorce found that 42% of divorcees say credit card debt and spending played a role in their divorce. Financial transparency isn't optional – it's protective.

The most effective structural approach for couples with different money styles: three accounts. One joint account for shared household expenses, and individual accounts for personal discretionary spending. Each partner contributes proportionally to the joint account. Personal spending comes from individual accounts, no explanation required.

The Money Date: A Monthly Budget Meeting That Actually Works

A Money Date is a scheduled, recurring conversation – 30 to 60 minutes – where both partners review the budget together. No phones, no distractions, no blame.

A practical agenda:

- Review – What did we spend last month? Where did we go over?

- Goals – What's the progress on our savings targets and debt payoff?

- Upcoming – What large expenses are coming next month?

- Adjust – Does anything in the budget need to change?

Financial psychologists recommend using "I" statements during disagreements ("I feel anxious when we overspend on dining out") rather than accusatory framing. The goal is alignment, not accountability court.

For couples navigating different spending philosophies, our guide on managing household finances without relationship conflict covers the full framework.

10+ Budgeting Tips and Strategies That Actually Work

These aren't theoretical. These are the behaviors that separate families who stick with a budget from those who quit after month two.

- Automate savings transfers on payday – the money moves before you can spend it

- Review your budget weekly, not monthly – a 10-minute weekly check-in catches problems before they compound

- Give every adult fun money – a fixed, no-questions-asked personal allowance prevents resentment

- Build sinking funds for every predictable irregular expense – car registration, holidays, back-to-school

- Use your actual spending history – pull 90 days of statements before setting any category limit

- Separate fixed and variable expenses – they require completely different management strategies

- Set a "24-hour rule" for unplanned purchases over $50 – wait a day before buying; impulse fades fast

- Involve all household decision-makers – budgets imposed by one partner fail at a significantly higher rate

- Review subscriptions quarterly – the average household carries $273/month in subscriptions per a 2025 C+R Research study, and most can't name half of them

- Celebrate milestones – when you hit your first $1,000 in savings, acknowledge it; the CFPB explicitly recommends recognizing progress to sustain motivation

- Adjust, don't abandon – one bad month is data, not failure; update the numbers and continue

- Track your debt-to-income ratio – use a DTI calculator to monitor how your debt load compares to income as you pay down balances

Budgeting strategies that work long-term share one trait: they're designed for real life, not ideal life. The families I see succeed aren't the ones with the most sophisticated spreadsheets. They're the ones who built a system they can maintain on a tired Tuesday evening.

Step 6 – Choose Your Budgeting Tools and Systems

Best Budgeting Apps for Families in 2026

According to a 2025 Academy Bank survey on banking trends, only 20.9% of Americans specifically use budgeting apps – but among those who do, the tools dramatically improve consistency. Forbes Advisor evaluated 38 budgeting apps on 18 data points for their 2026 rankings.

YNAB – Best for Zero-Based Budgeting

Cost: ~$99/year or $14.99/month. YNAB (You Need A Budget) runs entirely on the zero-based budgeting method: every dollar gets assigned a job before you spend it. The platform syncs with bank accounts automatically and tracks goals, debt payoff progress, and spending reports.

YNAB's own data shows new users save an average of $600 in the first two months and over $6,000 in the first year. The learning curve is real – plan two to three hours to set it up properly. After that, daily use takes under five minutes.

Mint – Best Free Option for Beginners

Note: Mint shut down in January 2024. Credit Karma (which acquired Mint's user base) now offers basic spending tracking. For full budgeting functionality, Monarch Money or EveryDollar are the recommended free-tier alternatives.

EveryDollar – Best for Dave Ramsey Followers

Cost: Free (manual entry) or ~$80/year for Ramsey+ with bank sync. EveryDollar is built around zero-based budgeting with a strong emphasis on debt elimination – the core of the Dave Ramsey Baby Steps framework. Shared access is available. Best for families whose primary financial goal is getting out of debt.

Monarch Money / Copilot – Best Premium Family Options

Monarch Money (~$100/year) is the strongest family-specific tool available. Multiple household members access one shared view – each with an individual login – while seeing the complete financial picture: checking, savings, investments, credit cards, and net worth. Rating: 4.8/5 in the App Store.

Copilot (~$95/year) leads on AI-powered expense categorization and design. It's exceptional for individual users who want automated insights. For multi-person household management, Monarch's shared architecture is more purpose-built. Rating: 4.8/5.

For families weighing digital tools against traditional spreadsheets, our full comparison at best budgeting tools for US families in 2025 walks through the tradeoffs in detail.

Budgeting Spreadsheets vs. Apps: Which Is Better for Families?

Spreadsheets win on customization and cost (free). Apps win on automation, real-time syncing, and reducing the manual burden that causes most people to quit.

The practical answer: if you'll actually open a spreadsheet every week, use it. If you know you won't maintain it manually, an app's automation is worth the subscription cost. The best budgeting tool is the one you open consistently.

Free Family Budget Templates: What to Look For

A good family budget template includes:

- Separate columns for income sources

- Pre-built categories for fixed, variable, and discretionary expenses

- A row for each sinking fund

- Monthly vs. annual view

- A net cash flow calculation at the bottom

The Bromoney budget planner is available on iOS and Android – built specifically for families tracking multiple income sources and shared expense categories.

App Comparison – Cost, Features, Family-Friendliness

| App | Annual Cost | Key Features | Joint Access | Platforms | User Rating | Best For |

|---|---|---|---|---|---|---|

| YNAB | ~$99/yr | Zero-based budgeting, goal tracking, debt payoff reports | YNAB Together | iOS, Android, Web | 4.7/5 | Families committed to zero-based budgeting |

| EveryDollar | Free / ~$80/yr (Ramsey+) | Zero-based, debt-elimination focus, Baby Steps integration | Yes | iOS, Android, Web | 4.7/5 | Debt-elimination-focused households |

| Monarch Money | ~$100/yr | Full financial dashboard, investments, net worth, goals | Multi-user profiles | iOS, Android, Web | 4.8/5 | Families wanting one view of all finances |

| Copilot | ~$95/yr | AI categorization, smart analytics, premium design | Yes | iOS, Android, Web | 4.8/5 | Analytics-focused individual users |

"While only 20.9% of respondents specifically use budgeting apps, our data shows a broader move toward digital tools for managing money." – Academy Bank, Banking Trends 2025

Research from Stanford University (2024) confirms that regular app use reduces impulse spending in families by 15-20% within the first three months. The critical variable: families who use automation features (auto-categorization, auto-transfers) maintain engagement significantly longer than those relying on manual entry. Per Fintech Global data, fewer than 25% of users remain active after 90 days – automation is what keeps the other 25% engaged.

Step 7 – Stick to Your Budget Without Feeling Miserable

Why Budgets Fail (And How to Prevent It)

Up to 65% of families abandon their budget within the first three months, according to 2025 financial counseling surveys. The cause is almost never math. It's design.

Budgets fail when they're built for an ideal version of life rather than the actual one. They fail when one partner controls the process and the other feels excluded. They fail when there's no room for spontaneity and no forgiveness for imperfection. Understanding why budgeting is important isn't the problem – execution is.

Build in Flexibility: The Wiggle Room Principle

Every budget needs a buffer category – call it "miscellaneous," "buffer," or "wiggle room." Allocate $50 to $150 per month here. This absorbs the small surprises (a birthday gift you forgot, a parking ticket, a co-pay) without breaking the entire plan.

Families that build in flexibility are significantly more likely to maintain their budget long-term. Rigid systems create fragility. Flexible systems create resilience.

The Power of No-Guilt Spending Categories

Certain categories should be off-limits for scrutiny: individual fun money, personal care, and small daily pleasures. When every dollar requires justification, the budget stops feeling like a tool and starts feeling like surveillance.

Define these categories explicitly. Set the limit. Then let go. The psychological safety of "guilt-free" spending zones protects the entire system.

How to Handle Budget Busters (Unexpected Expenses)

When an unexpected expense hits – a medical bill, a car repair, an appliance failure – the response determines whether your budget survives.

Step 1: Use your emergency fund if the expense qualifies (true emergency, not a want). Step 2: If no emergency fund exists, pull from the lowest-priority sinking fund or discretionary category this month. Step 3: Rebuild the depleted fund over the next two to three months.

If you're consistently hitting true emergencies without a fund to cover them, that's the signal to prioritize emergency savings above all other financial goals. Our emergency loans page covers short-term bridge options for situations where savings aren't yet in place – but building the fund eliminates the need for those options over time.

Monthly Budget Check-In: The Family Money Date Ritual

Schedule 30 minutes at the end of every month. Review every category. Celebrate what worked. Identify what didn't. Adjust the next month's allocations accordingly.

This ritual is the single most powerful predictor of long-term budget success. McGraw Hill's financial literacy research identifies "tracking without reviewing" as one of the top budgeting mistakes – families log spending but never analyze it or update their plan. The SD Financial Literacy Center recommends tracking expenses at least weekly and reviewing patterns monthly to catch structural problems before they compound.

Adjust, Don't Abandon: What to Do When the Budget Breaks Down

Only 15% of families follow their budget perfectly every month. The other 85% have months where something breaks. That's not failure – that's normal.

When a month goes off-plan, run a brief post-mortem: What specific category overspent? Was it a one-time event or a structural problem? Adjust the next month's allocation accordingly. Then move forward.

Quitting after one bad month is the budgeting equivalent of abandoning a diet after one slice of cake. The cake happened. The diet continues.

Common Family Budgeting Mistakes to Avoid

Mistake 1 – Making the Budget Too Restrictive

A budget that eliminates every discretionary dollar is a budget you'll quit. The research is consistent: overly restrictive financial plans trigger the same psychological response as crash diets. One slip feels like total failure, and the whole system gets abandoned.

Build in fun money. Build in flexibility. A budget that allows for $40 in personal spending per week is a budget you can maintain for years.

Mistake 2 – Forgetting Irregular Expenses

The average American family faces approximately $3,500 per year in irregular but predictable expenses – car registration, annual insurance premiums, back-to-school costs, holiday gifts, home maintenance. These aren't surprises. They're predictable costs on an unpredictable schedule.

The fix is sinking funds. Identify every annual or irregular expense, divide by 12, and add that amount as a monthly budget line. Our guide to separating one-time vs. recurring expense categories walks through exactly how to build this into your plan.

Mistake 3 – Not Having an Emergency Fund First

About 40% of American households cannot cover a $1,000 unexpected expense from savings, per a 2026 U.S. News Financial Wellness Survey. Without an emergency fund, a single car repair or medical bill forces a credit card charge – which adds interest, increases monthly debt payments, and shrinks the budget for everything else.

Build a starter emergency fund of $1,000 before aggressively paying down debt. Then grow it to three to six months of expenses. This single step prevents more budget collapses than any other action. The CFPB's emergency fund guide describes an emergency fund as "a cash reserve specifically set aside for unplanned expenses or financial emergencies" – and frames it as the foundation of any financial plan, not an optional add-on.

Mistake 4 – Not Involving All Decision-Makers

A budget built by one partner and imposed on another doesn't work. Financial transparency and shared ownership of the plan are non-negotiable for households with two adults.

A Debt.com survey found that 42% of divorced couples say spending and credit card debt contributed to their divorce. Financial infidelity – hiding purchases or accounts – is cited by more than a third of respondents. The Money Date ritual (monthly budget review together) is the structural solution.

Mistake 5 – Giving Up After One Bad Month

Statistically, the families who maintain a budget long-term are not the ones who never overspend. They're the ones who overspend, notice it, understand why, and adjust. The budget is a process, not a performance.

Real Family Budget Examples (See What Works)

Sample Budget: Family of 4 on $60,000 per Year

Monthly net income: approximately $4,200 (after taxes and deductions)

| Category | Monthly Amount | % of Net Income |

|---|---|---|

| Housing (rent/mortgage) | $1,400 | 33% |

| Transportation | $630 | 15% |

| Groceries | $714 | 17% |

| Healthcare & insurance | $588 | 14% |

| Childcare / school | $420 | 10% |

| Savings (emergency fund) | $210 | 5% |

| Fun money & misc. | $238 | 6% |

| Total | $4,200 | 100% |

At this income level, savings are tight. Priority one is a $1,000 starter emergency fund. Debt payoff and retirement contributions come after that foundation is in place.

Sample Budget: Dual-Income Family Earning $100,000+

Monthly net income: approximately $6,800 (based on $120,000 gross, after taxes)

| Category | Monthly Amount | % of Net Income |

|---|---|---|

| Housing | $2,040 | 30% |

| Transportation | $1,020 | 15% |

| Groceries & dining | $850 | 12.5% |

| Healthcare | $476 | 7% |

| Savings & investments | $1,020 | 15% |

| Childcare / activities | $680 | 10% |

| Discretionary / fun | $714 | 10.5% |

| Total | $6,800 | 100% |

At this income level, the 15% savings target is achievable. Both retirement contributions and a 529 plan can run simultaneously.

Sample Budget: Single-Income Family with Three Kids

Monthly net income: approximately $5,400 (based on $85,000 gross)

| Category | Monthly Amount | % of Net Income |

|---|---|---|

| Housing | $1,620 | 30% |

| Children's expenses (childcare, activities, school) | $1,134 | 21% |

| Groceries & transportation | $1,080 | 20% |

| Healthcare & insurance | $810 | 15% |

| Savings & emergency fund | $540 | 10% |

| Discretionary | $216 | 4% |

| Total | $5,400 | 100% |

This scenario requires the most discipline. Discretionary spending is minimal. Sinking funds for irregular expenses are critical – without them, any unexpected cost hits the savings category directly.

Frequently Asked Questions About Family Budgeting

How much should a family of 4 spend on groceries per month?

According to USDA food cost data for 2026, a family of four on a moderate-cost food plan spends $1,350-$1,600 per month on groceries. Families on a thrifty plan can target $900-$1,100 with meal planning, generic brands, and reduced dining out.

What is a realistic budget for a family of 4?

On a $60,000 annual income (approximately $4,200/month net), a realistic budget allocates roughly $1,400 to housing, $700 to transportation, $700 to groceries, and $600 to healthcare and insurance – leaving limited room for savings and discretionary spending. The 50/30/20 framework works as a starting guide, adjusted for actual local costs.

How do I start a family budget with my spouse if we disagree on money?

Start with goals, not numbers. Identify two or three financial outcomes you both want – a vacation, a paid-off car, a home. Build the budget backward from those shared goals. Use the three-account system (joint + individual accounts) to preserve personal autonomy while funding shared priorities. Schedule a Money Date to review progress monthly.

What percentage of income should go to housing for a family?

The standard guideline is no more than 28-30% of gross monthly income for housing costs (rent or mortgage payment, property taxes, and insurance). In high-cost cities, many families exceed this – if housing consumes 35%+, compress other discretionary categories and prioritize income growth.

How do I budget for kids activities without overspending?

Allocate 5-10% of your discretionary income to children's activities. Involve your kids in choosing one or two priority activities per season rather than saying yes to everything. Look for school-based programs, community center options, and used equipment to reduce costs. This is also a natural opportunity for teaching kids about money and budgeting – letting them participate in the tradeoff decision builds financial literacy early.

What is the best budgeting app for families?

Monarch Money leads for multi-person household management, offering shared access with individual profiles and a complete financial dashboard. YNAB leads for families committed to zero-based budgeting. EveryDollar is strongest for debt-elimination-focused households. The Bromoney budget planner (iOS / Android) is designed for families tracking multiple income sources and shared categories.

How long does it take to get used to a family budget?

Research consistently points to 90 days – three full monthly budget cycles – as the point where budgeting shifts from effortful to habitual. The first month is data collection. The second is adjustment. By the third, the categories feel natural and the process takes under an hour per month.

Popular Budgeting Techniques: Envelope Method, Zero-Based Budgeting, and More

| Method | Core Principle | Best Fit | Complexity | Flexibility | Key Advantage | Key Limitation |

|---|---|---|---|---|---|---|

| 50/30/20 Rule | 50% needs / 30% wants / 20% savings | Stable-income beginners | Low | Medium | Fast to implement, easy to explain | Breaks down when "needs" exceed 50% |

| Zero-Based Budgeting | Income - all allocations = $0 | Variable income; debt payoff | High | High | Maximum spending awareness | Time-intensive monthly setup |

| Envelope Method | Cash (or digital sub-accounts) per category | Impulse spenders; visual learners | Medium | Low | Hard stop on overspending | Inconvenient for cards/online |

| Pay Yourself First | Save first; spend the rest | Stable income; savings-focused | Low | High | Automates savings behavior | May underfund essentials if % is too high |

| 6 Jars / Accounts | 6 accounts at fixed percentages (55/10/10/10/10/5) | Holistic financial planners | Medium | Medium | Covers all financial dimensions | Rigid structure doesn't fit all income levels |

On zero-based budgeting specifically: the most common question is about the drawback of this method. The answer is decision fatigue. Assigning every dollar a job at the start of every month requires significant cognitive effort – especially in households with variable income. Families who use zero-based budgeting successfully pair it with automation (auto-transfers, auto-categorization in YNAB) to reduce the manual load. For a head-to-head comparison of these two leading approaches, see our full analysis at 50/30/20 vs. Zero-Based Budgeting.

Family Financial Planning: Tips for Managing a Shared Budget

Shared finances work when both partners operate from the same information. Secrecy – even unintentional secrecy, like not mentioning a subscription renewal – erodes trust and creates friction. Family financial planning is as much about communication as it is about spreadsheets.

Three structural practices that consistently improve shared budget management:

Shared visibility. Both partners should see every account, every transaction, every balance. Monarch Money and YNAB Together both support this natively. Surprises are the enemy of shared financial planning.

Proportional contribution to shared expenses. If one partner earns $70,000 and the other earns $40,000, contributing equally to shared bills creates disproportionate burden. Proportional contribution – each partner funds shared expenses at the same percentage of their income – is more equitable and reduces resentment.

Scheduled reviews, not reactive conversations. Money conversations that happen only when something goes wrong are almost always stressful. Monthly Money Dates shift the conversation from reactive to proactive.

"Three in four Americans (75%) say they've become more careful with money." – YouGov, What Americans Think About Saving, Budgeting and Debt, 2025

The trend toward financial caution is real. But caution without a system doesn't produce results. The system is the budget. And budgeting is important not because it restricts spending – but because it makes spending deliberate.

How to Effectively Manage a Home Budget

Home budgeting differs from a general personal budget in one key way: it must account for the physical costs of maintaining a household – maintenance, repairs, appliances, and seasonal expenses that renters don't face.

Homeowners should allocate 1-2% of their home's value annually for maintenance and repairs. On a $300,000 home, that's $3,000-$6,000 per year, or $250-$500 per month in a sinking fund. This number feels large until the water heater fails or the roof needs patching.

Track home expenses separately from general household expenses. This creates a clear picture of the true cost of homeownership and prevents maintenance costs from appearing as "surprises" in the monthly budget.

For families carrying high-interest debt alongside a mortgage, tracking your credit utilization is a useful parallel habit – it shows how your revolving debt compares to available credit, which directly affects your borrowing costs.

What Is Capital Budgeting (And How It Differs from Your Monthly Budget)?

Capital budgeting, in the context of personal and family finance, is the process of analyzing and planning for large, long-term financial commitments – a home purchase, a vehicle replacement, a private school education, or a major home renovation.

It differs from your operational monthly budget in scope and time horizon. Your monthly budget manages recurring income and expenses. Capital budgeting evaluates whether a major purchase makes financial sense over a multi-year period – considering total cost of ownership, financing options, opportunity cost, and long-term impact on household cash flow.

Families use capital budgeting principles when deciding: Should we buy or lease a car? Does it make sense to buy a home now, or rent for two more years? Is the cost of a private school education worth the financial strain?

The discipline mirrors corporate capital budgeting: weigh the full cost, evaluate the alternatives, model the impact on your financial position, and make a deliberate decision rather than an emotional one.

Next Steps: Build on Your Family Budget

A budget is a foundation, not a destination. Once your monthly spending plan is running, the next layer of financial stability comes from building on it systematically.

Internal resources to explore next:

- Teaching kids about money and budgeting – how to involve children in the family financial conversation at every age

- Best budgeting tools for US families in 2025 – full comparison of apps vs. spreadsheets

- Why fun money is non-negotiable for budget stability – the behavioral case for personal spending allowances

- Avoiding budget blindness from over-automation – how to stay engaged when everything runs on autopilot

- Managing household finances without relationship conflict – the three-account system and Money Date framework in depth

- Separating one-time vs. recurring expense categories – why this distinction is the foundation of accurate budgeting

- 50/30/20 vs. Zero-Based Budgeting: Full Comparison – which method fits your family's income structure

Tools and calculators:

- Debt payoff calculator – model how extra monthly payments accelerate your debt-free date

- DTI calculator – understand your debt-to-income ratio and how it affects loan eligibility

- Credit utilization calculator – track how your revolving balances affect your credit score

When the budget reveals a cash flow gap:

If your expense tracking surfaces a real shortfall – not a planning error, but a genuine gap between income and necessary expenses – personal loans and installment loans are structured options worth evaluating alongside your budget plan. Use them as a bridge, not a substitute for the plan itself.

Denis Goncharenko

Managing Editor & FinTech Content Strategist

Editorial Policy: Denis ensures every financial claim is backed by institutional data sources.

Was this article helpful?

Same blogs

The Envelope Method's Hidden Traps: When Your Budget Creates a False Sense of Financial Security

The envelope method feels like control. But in reviewing household budgets, the same pattern keeps appearing: people who follow their envelopes religiously and still end up in financial crisis. Here's why the envelopes were full while the financial picture was not.

How to Allocate Budget Categories for a Family Making $40,000–$60,000 a Year

A family earning $40,000–$60,000 a year sits well below the $83,730 U.S. median household income – but a structured budget makes financial stability achievable. This guide breaks down every major spending category by percentage and dollar amount, with sample monthly templates for three income levels and a prioritized savings and debt-payoff sequence built for 2026 tax parameters.

Digital Envelope Apps vs. Physical Cash Envelopes: Which Budgeting System Is Right for You?

About 15% of active budgeters use the envelope method – 11% go digital, only 4% stick with cash. This guide breaks down exactly how each system works, where each one fails, and how to pick the one that fits how you actually spend money.