Budgeting as a Couple When You Live Together: A Conflict-Free Guide

Living together reshapes your finances overnight. Two separate cash flows, two sets of habits, and two different definitions of "too expensive" now share the same kitchen table. According to the Fidelity 2024 Couples & Money Study, 45% of partners admit they argue about money at least occasionally – and nearly 9 in 10 of those same couples believe their communication is "good." That gap between perception and reality is exactly where conflicts are born.

This guide walks you through every stage of building a shared budget: from the first honest conversation to choosing a model that fits your income split, picking the right tools, and setting goals you'll actually hit together. For a broader foundation, start with our overview of building a harmonious family budget.

Why Money Is the #1 Source of Conflict for Couples

The Data Behind the Fights

Financial disagreements aren't just common – they're structurally predictable. Research published through the American Association for Marriage and Family Therapy (2024) found that 56% of couples argue about money, and financial stress measurably lowers relationship satisfaction. Separate analysis in behavioral finance literature puts financial issues as a factor in 20–40% of breakups and divorces.

The mechanism is rarely about the dollar amount itself.

"Conflicts about money are almost never really about the money. They're about what money represents – security, power, freedom, values, and love." – Dr. John Gottman, founder of The Gottman Institute

Dr. Brad Klontz, financial psychologist and co-founder of the Financial Psychology Institute, adds a structural explanation: partners arrive with opposing "money scripts" absorbed in childhood – one grew up in a household where saving felt like survival, the other where spending felt like celebration. Those scripts collide silently until the credit card statement arrives.

There's also a stress-avoidance loop at work. Research published in the Journal of Family and Economic Issues (2023) shows that the more financially stressed a person feels, the less likely they are to initiate money conversations with their partner – precisely because they anticipate conflict. The silence compounds the problem.

"Financially stressed individuals are less likely to discuss money with their romantic partners… it is the anticipated fear of conflict that prevents individuals from addressing the elephant in the room." – Garbinsky & Gladstone, Journal of Consumer Research

Dr. Terri Orbuch, sociologist and lead researcher on the Early Years of Marriage Project at the University of Michigan, puts the stakes plainly:

"In my longitudinal research, arguments about money turned out to be the single strongest predictor of divorce – regardless of income level or net worth."

A March 2024 Bankrate survey found that 47% of U.S. adults say money negatively affects their mental health. Among them, 59% cite difficulty covering everyday expenses as the top driver. That number isn't abstract – it's what happens when two people move in together without a shared system for managing money.

The takeaway: the problem isn't the money. It's the absence of a shared system for managing it together.

Start Here: The First Money Conversation

Questions Every Couple Should Cover Before Combining Finances

A University of Georgia couples study (2023) found that couples who had open conversations about money and agreed on their approach were 105% more likely to combine accounts – which correlated with greater relationship stability. That first conversation doesn't need to be a formal audit. It needs to be honest.

Cover these topics before deciding on any model or opening any shared account.

| Topic | Sample Question | Goal of the Discussion |

|---|---|---|

| Income | "What does each of us bring home monthly after taxes?" | Establish the total household cash flow available for planning |

| Debt & credit | "Do either of us carry student loans, credit card balances, or other obligations? What are the monthly payments?" | Map total debt load and build a repayment strategy |

| Savings | "How much do we each have saved, and what is it earmarked for?" | Assess current financial cushion and align savings targets |

| Biggest expenses | "Where does most of our money go right now? What's fixed vs. flexible?" | Identify cost drivers and find optimization opportunities |

| Budget model | "Do we want fully shared finances, fully separate, or a hybrid?" | Choose a structure both partners are genuinely comfortable with |

| Financial goals | "What do we want to accomplish together in the next one to five years?" | Align direction so spending decisions reinforce shared priorities |

| Money attitudes | "How do you feel about risk, spontaneous purchases, and saving for the future?" | Surface conflicting money scripts before they cause friction |

| Big-purchase threshold | "At what dollar amount should a purchase require a joint conversation?" | Set a clear rule that prevents unpleasant surprises |

| Investing | "Have either of us invested before? What level of risk feels acceptable?" | Establish a starting investment framework |

| Family obligations | "Do either of us support parents or other relatives financially?" | Make those commitments visible in the shared budget |

In my experience reviewing household financial setups, couples who skip the debt and family-obligation rows almost always revisit them under worse conditions – usually after a missed payment or an unexpected wire transfer that "came out of nowhere." Those two rows aren't optional.

Three Budget Models for Couples

There is no universal right answer here. The best budgeting model is the one both partners will actually follow. Each approach has a distinct logic, and the right choice depends on income parity, trust level, and how each person relates to financial independence.

Fully Merged Budget

All income flows into a single joint account. All expenses – rent, groceries, streaming subscriptions, date nights – come out of that same pool. This is the classic "our money" model.

Works best when: both partners share similar spending values, have comparable long-term goals (mortgage, children), and maintain a high level of mutual trust and open communication.

Advantages: maximum transparency, simple accounting, strong sense of financial unity. Research published in the Journal of Consumer Research (2023) shows fully pooled couples score a median relationship satisfaction of 6.10 out of 7.0 – the highest of the three models. Couples with shared finances report greater satisfaction with their relationships, likely because joint accounts create both transparency and shared responsibility.

Risks: loss of individual financial autonomy, potential for one partner to exert disproportionate control, and real complexity when separating assets if the relationship ends. For couples who value independence, this model can feel suffocating within months.

Fully Separate Budget

Each partner manages their own income and accounts independently. A shared account exists solely for joint obligations – rent, utilities, shared subscriptions – funded either 50/50 or proportionally to income.

According to YouGov's 2026 couples finance survey, up to 44% of Millennial and Gen Z couples in the U.S. operate on separate or hybrid models, compared to just 13–15% of older generations. The U.S. Census Bureau data shows the share of married couples with no joint accounts rose from 15% in 1996 to 23% in 2023 – a structural shift in how Americans approach budgeting with a partner.

Advantages: financial independence, protection from a partner's debt, fewer arguments about discretionary spending habits.

Risks: can create emotional distance – the "roommates" dynamic – and makes long-term planning harder. When one partner steps back from work for parental leave or illness, the model amplifies inequality fast. Research consistently shows that people who keep finances entirely separate report lower relationship satisfaction than those who pool at least some resources.

Hybrid Model: "Yours, Mine, and Ours"

This is the most widely adopted structure among couples under 35. Roughly 65% of that age group use some version of it, per financial behavior reports from 2024–2026.

Each partner maintains a personal account for individual expenses. Both contribute to a shared account that covers household obligations. Contributions are either equal or proportional to income – more on that calculation below.

The California Department of Financial Protection and Innovation (DFPI) specifically recommends this structure, noting that separate fun money accounts for individual purchases – clothing, entertainment, personal hobbies – eliminate the need to "ask permission" for everyday spending choices. That psychological shift matters more than most couples expect.

In our experience at Bromoney reviewing how households actually manage money together, the hybrid model succeeds most consistently when the shared contribution amount is set based on actual joint expenses – not a round number that sounds fair in theory but leaves one partner short every month.

How to Split Expenses Fairly

The 50/50 Method

Each partner pays half of every shared expense.

Example: Combined monthly household costs of $3,200 → each pays $1,600.

Pros: simple math, creates a clear sense of equality.

Cons: ignores income disparity. If one partner earns $90,000 and the other earns $40,000, equal dollar contributions represent very different percentages of take-home pay – and the lower earner has almost nothing left for personal savings or debt repayment. YouGov's 2026 data shows that even among couples where one partner earns "a lot more," 33% still split 50/50 – a setup that research consistently links to suppressed resentment over time.

Proportional Split

Each partner contributes a share of joint expenses equal to their share of total household income. Financial advisors recommend this method for couples budgeting together with a significant income gap – it leaves both partners with a comparable proportion of personal money after obligations.

Formula: (Your income ÷ Combined household income) × Total shared expenses = Your contribution

Example: Partner A earns $6,000/month (60% of household income). Partner B earns $4,000/month (40%). Total shared expenses: $4,800/month.

- Partner A contributes: $2,880

- Partner B contributes: $1,920

Both partners retain roughly the same proportion of their personal income after obligations – which is the point.

Pros: financially equitable, leaves each partner with comparable discretionary money, reduces the quiet resentment that builds when one person consistently carries more.

Cons: requires full income transparency, which some couples find uncomfortable early in the relationship.

Among couples with a significant income gap, approximately 65% use proportional splitting, per 2024–2025 behavioral finance surveys. The psychological benefit extends beyond math: when both partners feel the system is fair, financial conversations become less adversarial and spending habits stop being a source of friction.

For couples carrying debt into a shared household, the Bromoney debt payoff calculator maps a payoff timeline across different monthly payment scenarios – which makes the proportional contribution conversation concrete rather than abstract.

Step-by-Step: Building Your Shared Budget

Creating a budget together follows a predictable sequence. Skip a step and the system develops a gap that shows up later as a conflict.

Step 1: Calculate Combined Income

Add every income source: salaries, freelance revenue, rental income, bonuses, and any benefits. Use after-tax figures. This is your real number – the one the budget is built on. Gross income looks better but doesn't pay rent.

Step 2: List All Expenses

Separate fixed obligations (rent or mortgage, car payments, insurance, utilities, minimum debt payments) from variable spending (groceries, dining, clothing, entertainment). Track every expense for one to two months before setting limits – most couples underestimate variable spending by 20–30%.

The 50/30/20 rule – 50% to needs, 30% to wants, 20% to savings – is a useful starting framework for zero-based budgeting, though most couples adjust the ratios based on debt load and goals. The rule's value is forcing a conversation about what counts as a "need" versus a "want" – a disagreement that surfaces money scripts fast.

Step 3: Allocate Savings First

Before distributing money to spending categories, set aside 10–20% of combined income for savings and investments. If you carry high-interest debt, redirect part of that allocation to accelerated payoff. Automating this transfer on payday removes the temptation to spend it first – and eliminates the monthly negotiation about whether there's "enough left over" to save.

Step 4: Fund the Emergency Reserve

Target 3–6 months of combined fixed expenses in a liquid, accessible savings account. This single step reduces financial stress more than almost any other budget decision. The Bankrate March 2024 financial stress survey found that 47% of U.S. adults report money negatively affecting their mental health – and the top driver (cited by 59%) is difficulty covering everyday expenses. A funded reserve eliminates that category of stress before it reaches the relationship.

For couples facing unexpected family emergency costs before the reserve is built, our guide on unexpected family emergency costs covers how to handle one-time expenses without derailing the long-term plan.

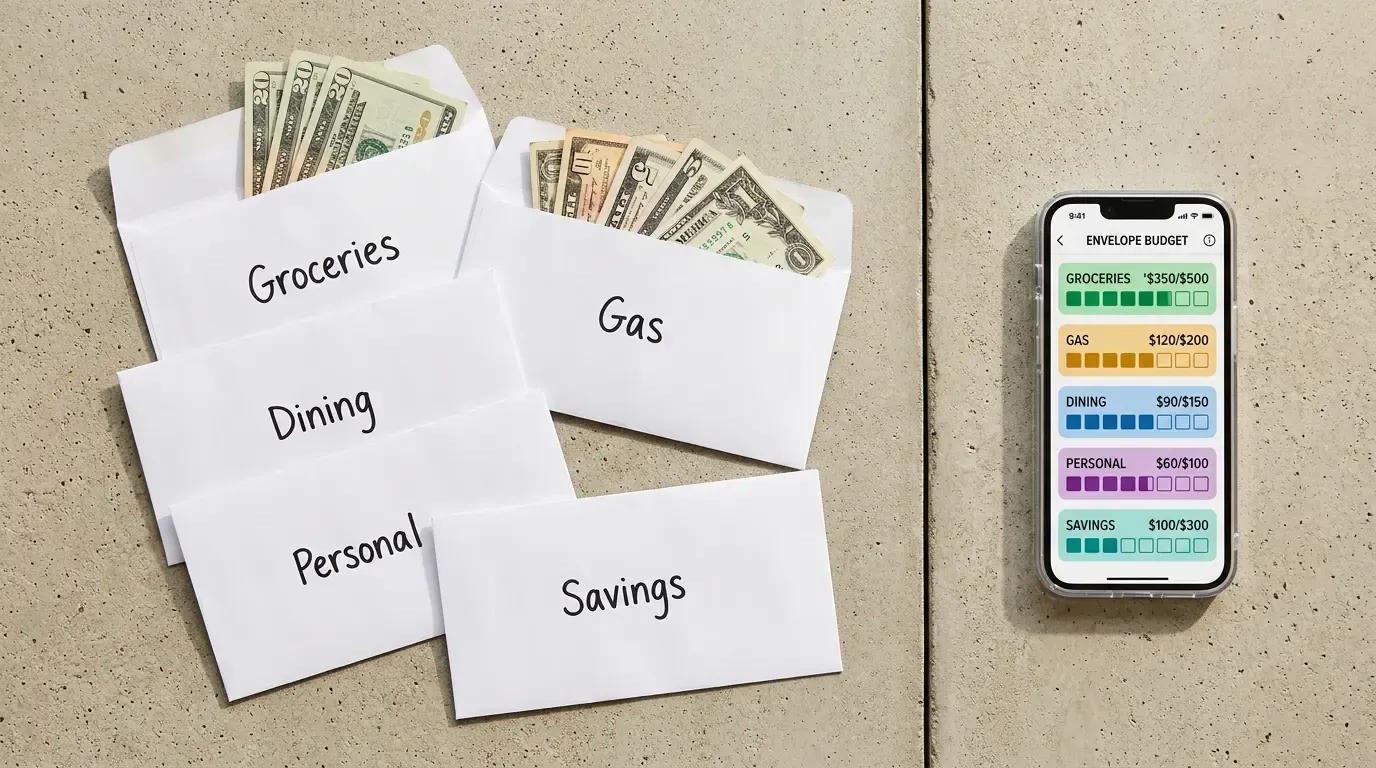

Step 5: Assign Spending Categories

Distribute the remaining income across variable categories with agreed monthly limits. Document this in a shared Google Sheet, a budgeting app, or a written agreement. The format matters less than the shared visibility – both partners need to see the same numbers in real time. This is where shared notification management becomes critical: when one partner owns all the autopay alerts and account access, the other becomes financially dependent without realizing it.

Step 6: Review Monthly

Set a fixed date – the first Sunday of the month works well for many couples. Review actual vs. planned spending, adjust limits where needed, and check progress toward savings goals. Monthly money dates keep the budget a living tool rather than a document that gets ignored after week two. Research published in Personal Finance & Planning (2023) found that couples who hold structured monthly financial check-ins report significantly fewer escalating conflicts than those who discuss money only when a problem surfaces.

Best Tools for Couples Budgeting Together

Apps Built for Shared Finances

The California DFPI explicitly recommends Honeydue, Goodbudget, and YNAB as purpose-built tools for couples managing shared finances. Here's how the current top options compare for couples budgeting in 2025–2026:

| App | Platform | Price | Key Features for Couples | App Store Rating |

|---|---|---|---|---|

| YNAB | iOS / Android / Web | ~$14.99/month | Zero-based budgeting method, shared goals, detailed reports | 4.8 ⭐ |

| Honeydue | iOS / Android | Free (Pro available) | Shared + individual balances, in-app chat, bill reminders | 4.7 ⭐ |

| Splitwise | iOS / Android / Web | Free (Plus available) | Expense splitting, debt tracking, group costs | 4.7 ⭐ |

| Goodbudget | iOS / Android / Web | Free / $10/month | Envelope budgeting method, shared envelopes across devices | 4.6 ⭐ |

| PocketGuard | iOS / Android | Free / $7.99/month | Real-time tracking, bill reminders, debt payoff plans | 4.6 ⭐ |

YNAB is the strongest choice for couples serious about financial discipline – it forces you to assign every dollar a job before spending it. The learning curve is real, but couples who commit to the zero-based budgeting method typically see spending clarity within 60 days.

Honeydue is purpose-built for couples and handles the "whose money is this?" question natively, with separate and shared balance views in one interface. It's the closest thing to a dedicated couples budgeting app on the market.

Splitwise is not a budgeting tool – it's a shared ledger for tracking who owes whom. Use it alongside a budget app, not instead of one. Treating Splitwise as a substitute for a real shared budget is one of the more common mistakes I see among couples who are new to managing money together.

For couples who prefer a low-tech approach, a shared Google Sheet with clearly labeled tabs (Income, Fixed Expenses, Variable Expenses, Savings Goals) works reliably. For a dedicated mobile option, the Bromoney Budget Planner – available on Google Play and the App Store – handles apps for split household expenses with a straightforward shared interface designed for couples new to joint budgeting.

Strategies to Prevent Financial Conflicts

What Actually Works

The research backing on structured money conversations is consistent. A 2023 analysis published in Personal Finance & Planning found that couples who hold monthly financial check-ins report significantly fewer escalating conflicts than those who discuss money only when a problem surfaces. Fidelity's 2024 guidance echoes this directly: "Consider setting aside a dedicated slot of time for your financial check-in so you can give the issues your full attention."

Here are the six strategies that show up repeatedly in both research and practice:

Regular money dates. Schedule a monthly sit-down – no phones, no TV – to review the budget, track progress toward savings goals, and surface any financial concerns before they compound. The goal isn't to audit each other; it's to stay aligned. Couples who treat this as a recurring calendar event rather than a reaction to problems report measurably lower conflict frequency.

Define shared goals. Write down two to three joint financial targets with dollar amounts and deadlines. A shared goal transforms budgeting from a constraint into a project. Without it, spending decisions pull in different directions and neither partner understands why the other is frustrated.

Use the hybrid structure. A joint account for shared obligations plus personal accounts for individual spending solves the "asking permission" problem structurally. Neither partner needs to justify a haircut or a video game purchase. The shared account covers what's shared; personal accounts cover everything else.

Guarantee personal "no-questions" money. Each partner receives a fixed monthly amount to spend without reporting or justification. Treat this as a non-negotiable line item in the budget, not a leftover. When personal spending money is guaranteed, the impulse to hide purchases drops sharply – and with it, most of the low-grade resentment that builds around discretionary spending habits.

Set a big-purchase rule. Any purchase above an agreed threshold – $200 to $500 is common – requires a joint conversation before buying. This single rule eliminates most of the "I can't believe you spent that" arguments without restricting either partner's autonomy below the threshold.

Maintain full financial transparency. Both partners know the real income figures, debt balances, and account totals. Financial secrets – even small ones – erode trust faster than almost any spending decision. The University of Georgia research found that couples who agreed on their financial approach were 105% more likely to combine accounts, and that transparency correlated directly with relationship stability.

Common Budgeting Mistakes Couples Make

What to Fix Before It Becomes a Fight

1. Hidden spending One partner makes purchases they don't disclose. The immediate damage is financial; the lasting damage is to trust. Fix: agree on a personal spending limit – $150/month per person is a common starting point – that requires zero explanation. Anything above the big-purchase threshold gets discussed first.

2. No emergency fund Without a buffer, any unexpected expense – a car repair, a medical bill, a job loss – forces the couple into debt or conflict. Target 3–6 months of fixed household expenses in a dedicated savings account. For situations where an emergency hits before the reserve is built, the Bromoney emergency loans page covers short-term options – but a funded reserve eliminates the need for most of them.

3. Ignoring personal money Couples who funnel everything into a joint account with no personal allocation often develop a sense of financial surveillance. Research from the DFPI confirms that separate accounts for individual discretionary spending reduce the "asking permission" dynamic that erodes autonomy over time. This isn't a luxury – it's a structural safeguard.

4. No shared financial goals Without goals, spending is reactive. Fix: set two to three specific, time-bound targets together. A SMART example: "Save $18,000 for a down payment by December 2027 by transferring $600/month to a dedicated high-yield savings account." The specificity matters – vague goals don't change behavior.

5. One partner controls all the money This creates financial illiteracy – and vulnerability – in the other partner. Both people should know where the accounts are, what the balances are, and how the budget works. Joint decisions, even if one person handles day-to-day execution. If one partner manages all the automated payments and account access, the other is one emergency away from being completely lost.

6. Skipping the monthly review Budgets become outdated fast. Income changes, expenses shift, goals evolve. A budget reviewed once at setup and never revisited is decoration. Monthly reviews keep it functional and keep both partners accountable to the same plan.

7. Splitting 50/50 when incomes differ significantly YouGov's 2026 data shows that in couples where one partner earns substantially more, 33% still split expenses equally – a setup that quietly builds resentment in the lower earner. Proportional splitting resolves this structurally. The math is straightforward; the harder part is having the income transparency conversation that makes the calculation possible.

A pattern that shows up repeatedly in practice: couples who skip the emergency fund and ignore the proportional split tend to hit the same two crises – one unexpected expense that triggers debt, and one partner who eventually says "I've been carrying more than my share." Both are preventable with the right system in place from the start.

For couples carrying existing debt into a shared household, the Bromoney debt payoff calculator helps map a payoff timeline before building the joint budget around it.

Setting Shared Financial Goals

Planning for Big Purchases and Building Reserves

Shared goals transform budgeting from a constraint into a project. The mechanics matter as much as the ambition – a goal without a monthly contribution amount and a target date is a wish, not a plan.

Use the SMART framework for every major target:

- Specific: "Save for a down payment on a home" beats "save more money"

- Measurable: "$24,000 in a dedicated savings account"

- Achievable: "By contributing $800/month from our combined income"

- Relevant: "So we can stop renting and build equity by 2027"

- Time-bound: "Target date: Q3 2027"

For medium-term goals – a car, a vacation, a home renovation – open a separate labeled savings account for each target. Visibility of progress is a stronger motivator than willpower alone. Automating the monthly transfer on payday removes the decision entirely and prevents the end-of-month "we already spent it" conversation.

The emergency fund is not a savings goal – it's a prerequisite. Build it to 3–6 months of fixed household expenses before aggressively funding any other target. Per the Bankrate 2024 survey, difficulty covering everyday expenses is the single most cited driver of financial stress in American households. The reserve eliminates that category of stress before it reaches the relationship.

For longer-horizon goals – retirement, a child's education, a rental property – consider tax-advantaged accounts: Roth IRA, 401(k) employer match, HSA. These compound the impact of saving without changing the monthly contribution amount. The earlier a couple aligns on long-term goals together, the more time compounding has to work. Our guide on explaining family finances to children covers how to bring kids into these conversations as the household grows.

Frequently Asked Questions

How do you split expenses fairly when incomes are very different?

Proportional splitting is the method financial advisors recommend for couples with a significant income gap. Divide each partner's income by combined household income to get their percentage, then multiply that percentage by total shared expenses.

Example: Partner A earns $7,500/month, Partner B earns $2,500/month. Combined: $10,000. Shared expenses: $4,000/month.

- Partner A pays 75% → $3,000

- Partner B pays 25% → $1,000

Both partners keep the same proportion of their personal income after contributions. Among couples with a large income disparity, approximately 65% use proportional splitting, per 2024–2025 behavioral finance research. The key condition: both partners should retain enough personal money after contributions to feel financially autonomous – not just mathematically solvent.

What is the best budgeting model for couples living together?

The hybrid model – joint account for shared expenses, personal accounts for individual spending – is the most widely adopted structure among couples under 35, used by roughly 65% of that demographic. Research published in the Journal of Consumer Research shows fully pooled finances correlate with the highest relationship satisfaction scores (6.10 out of 7.0), but the hybrid model scores nearly as well (5.82 out of 7.0) while preserving individual autonomy. The right model depends on income parity, trust level, and how each partner relates to financial independence.

How often should couples review their budget together?

Monthly. A fixed calendar date – same day each month – works better than "whenever we remember." The review should cover actual vs. planned spending, progress toward savings goals, upcoming large expenses, and any adjustments to contribution amounts. Research consistently shows that regular structured check-ins reduce the frequency of escalating financial conflicts compared to ad hoc discussions triggered by problems.

What budgeting apps work best for couples in 2026?

YNAB leads for couples committed to detailed financial planning – the zero-based budgeting method forces clarity that most couples don't have until they try it. Honeydue is purpose-built for couples and handles shared and individual balances in one view. Goodbudget applies the envelope method to shared spending. For couples who primarily need to track shared expenses and settle debts, Splitwise works well as a complement to a full budgeting tool. The Bromoney Budget Planner (App Store / Google Play) is built specifically for households managing split expenses and shared goals.

How do you handle one partner's debt in a shared budget?

Debt brought into the relationship stays legally individual unless you refinance jointly. But it affects the shared budget – it reduces that partner's available contribution. The transparent approach: disclose all outstanding balances before finalizing any shared budget model. Then decide together whether to accelerate payoff using shared savings, or treat it as a personal line item funded from that partner's personal account. The Bromoney debt payoff calculator maps payoff timelines across different monthly payment scenarios, which makes the conversation concrete rather than abstract.

Should couples explain their budget structure to their kids?

Age-appropriate financial transparency builds money literacy early. Explaining how the household budget works – without burdening children with adult financial stress – is a meaningful first step. Our guide on explaining family finances to children covers how to frame these conversations by age group.

What if one partner manages all the notifications and automated payments?

Shared visibility matters as much as shared contribution. When one partner owns all the shared notification management – autopays, alerts, account access – the other partner becomes financially dependent without realizing it. Both people should have login access to every shared account and at least a monthly view of automated transactions.

The data cited in this article draws from the Fidelity 2024 Couples & Money Study, Bankrate's March 2024 financial stress survey, YouGov's 2026 couples finance report, the University of Georgia's couples and financial pooling research, and publications from the American Association for Marriage and Family Therapy. All dollar figures are in USD unless otherwise noted.

Denis Goncharenko

Managing Editor & FinTech Content Strategist

Editorial Policy: Denis ensures every financial claim is backed by institutional data sources.

Was this article helpful?

Same blogs

The Envelope Method's Hidden Traps: When Your Budget Creates a False Sense of Financial Security

The envelope method feels like control. But in reviewing household budgets, the same pattern keeps appearing: people who follow their envelopes religiously and still end up in financial crisis. Here's why the envelopes were full while the financial picture was not.

How to Allocate Budget Categories for a Family Making $40,000–$60,000 a Year

A family earning $40,000–$60,000 a year sits well below the $83,730 U.S. median household income – but a structured budget makes financial stability achievable. This guide breaks down every major spending category by percentage and dollar amount, with sample monthly templates for three income levels and a prioritized savings and debt-payoff sequence built for 2026 tax parameters.

Digital Envelope Apps vs. Physical Cash Envelopes: Which Budgeting System Is Right for You?

About 15% of active budgeters use the envelope method – 11% go digital, only 4% stick with cash. This guide breaks down exactly how each system works, where each one fails, and how to pick the one that fits how you actually spend money.