Age & Residency

Must be at least 18 years old and a legal U.S. resident or citizen with a valid government-issued ID.

South Dakota borrowers can apply for personal loans online and receive offers from direct lenders - without leaving home. Bromoney matches you with lenders who fit your financial profile, whether you need funds for an emergency, home repair, or debt consolidation. Submit one request and compare real terms today.

No impact to your credit score to check.

Get StartedSecure 256-bit Connection

A personal loan is an unsecured installment loan, meaning no collateral is required. It provides a lump sum that you repay over a fixed term (typically 24 to 84 months) with a predictable, fixed interest rate. Lenders determine your APR based on credit score, income, and debt-to-income ratio (DTI). Borrowers with strong credit access the best rates, while options exist for those with lower scores.

Many South Dakota lenders disburse approved personal loan funds via ACH within one business day - sometimes the same day for morning applications.

South Dakota's open lending market means lenders assess more than your credit score. Income, employment history, and monthly cash flow all count toward approval - giving borrowers with imperfect credit a real shot at qualifying.

Every lender in Bromoney's network serving South Dakota must hold a valid license issued by the South Dakota Division of Banking and comply with SDCL Title 54 disclosure requirements.

The request may take a few minutes. Here's what most South Dakota lenders require before they can review your information and decide whether to offer credit.

Must be at least 18 years old and a legal U.S. resident or citizen with a valid government-issued ID.

Proof of steady income (e.g., W-2s, self-employment records, or benefits) is needed to assess your repayment ability and DTI ratio.

A valid U.S. checking or savings account is necessary for receiving funds and making scheduled monthly payments.

Legal lending restrictions for SD residents.

Max Loan Amount

Based on South Dakota statutes - lenders set individual limits

Max Term

Maximum allowed repayment window set by individual lender agreement

APR/Fees

South Dakota imposes no general usury ceiling on consumer personal loans (SDCL 54-3)

Rollovers

South Dakota law does not expressly prohibit the refinancing of a personal loan, but rollover terms must be disclosed in the original loan agreement per SDCL Title 54 requirements.

Information provided is for educational purposes only. Borrowers are encouraged to review all loan terms carefully before signing. Interest rates and fees vary by lender and loan type.

Unlike neighboring Minnesota, which caps payday and small-dollar loan rates, or North Dakota, which also maintains a permissive lending environment but applies its own licensing and disclosure requirements to consumer lenders, South Dakota places no rate ceiling on personal loans. This draws a larger pool of active lenders to the state, which increases borrower choice but also requires closer comparison of competing offers before signing.

Consumer lending in South Dakota is regulated by the South Dakota Division of Banking (Department of Labor and Regulation). The Division licenses all consumer lenders, enforces SDCL Title 54 disclosure rules, and accepts borrower complaints at dlr.sd.gov. Borrowers can verify a lender's license status through the Division's online registry before signing any loan agreement.

Jordan T.

“The application flow was clear and I knew exactly what to prepare before submitting. Funds reached my account the next business day.”

Monica R.

“I used the resources and calculators first, then compared options with much more confidence. The APR breakdown made the math obvious.”

Devon K.

“Their pre-qualification flow showed me three lenders with no origination fee — I would have missed that on my own.”

Priya S.

“Every offer showed APR and total repayment cost up front. No hidden fees in the fine print.”

Andre L.

“I expected to get rejected with my score, but two partner lenders responded with available terms.”

South Dakota's lending laws under SDCL Title 54 require lenders to disclose all fees and terms upfront before a borrower signs. Bromoney surfaces only licensed lenders who meet those disclosure standards, so residents compare real, complete offers - not teaser rates that change at signing. One form, multiple competing options, zero guesswork.

Estimate exactly how much you'll owe before you commit. Enter your loan amount and repayment term to see total costs, including fees and interest, laid out clearly.

Calculate my loanBorrow against your home's equity for lower rates, but your property is at risk.

Instant access to cash from your credit line, but high fees and interest apply immediately.

Personal loan terms, APRs, and amounts vary by state. California, for instance, caps APRs on certain loans. Other states like Florida and Texas have distinct licensing rules that impact lender availability and terms. Before applying, review your state's regulations to understand the local lending landscape.

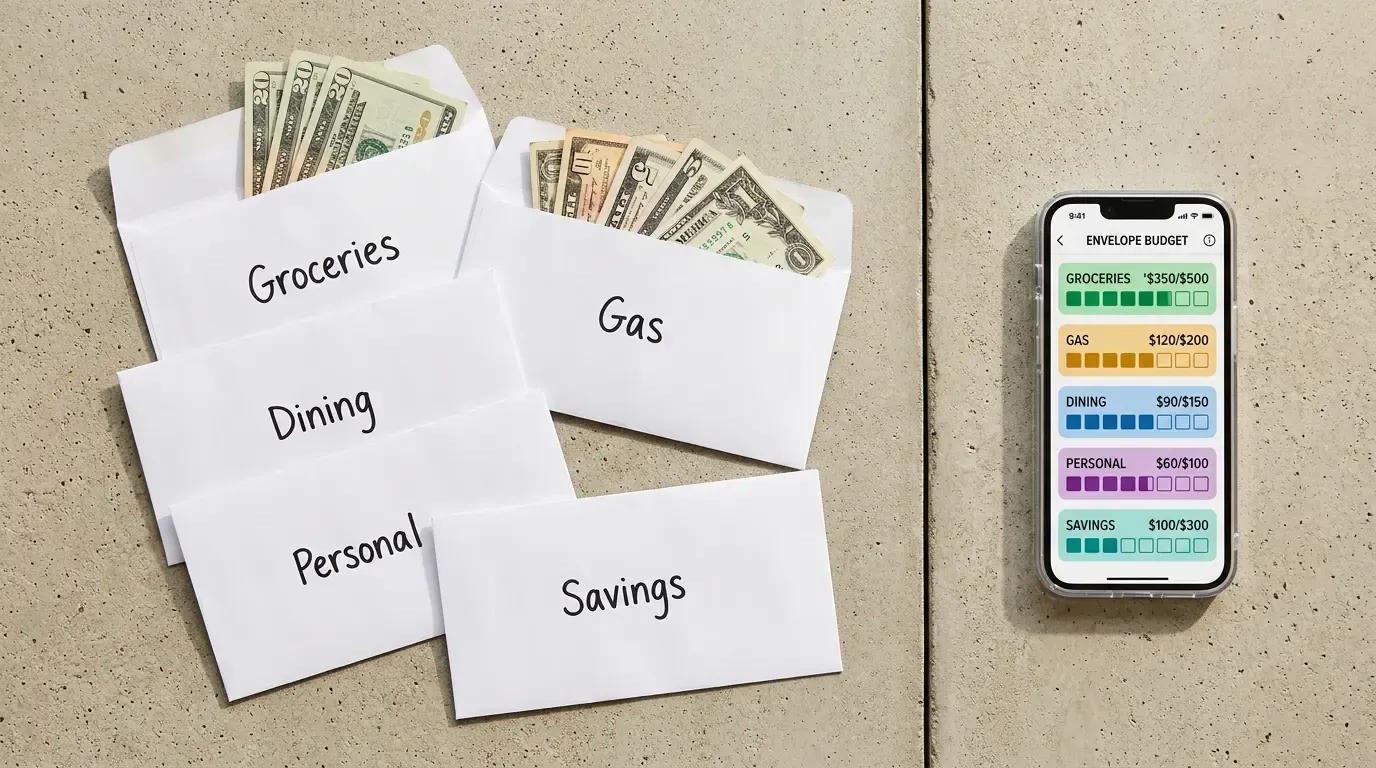

The envelope method feels like control. But in reviewing household budgets, the same pattern keeps appearing: people who follow their envelopes religiously and still end up in financial crisis. Here's why the envelopes were full while the financial picture was not.

A family earning $40,000–$60,000 a year sits well below the $83,730 U.S. median household income – but a structured budget makes financial stability achievable. This guide breaks down every major spending category by percentage and dollar amount, with sample monthly templates for three income levels and a prioritized savings and debt-payoff sequence built for 2026 tax parameters.

About 15% of active budgeters use the envelope method – 11% go digital, only 4% stick with cash. This guide breaks down exactly how each system works, where each one fails, and how to pick the one that fits how you actually spend money.

We bridge the gap between your financial goals and premier lending services nationwide.

This page is informational and does not guarantee approval. Actual rates depend on your lender and South Dakota regulations.

Join millions of Americans who trust our platform to compare rates, find the best loans, and rebuild their credit — all in one place

Submitted over a secure connection