Psychology of Cash: Why Physical Money Feels 'Real'

Every time you hand over a $20 bill, something happens in your brain that doesn't occur when you tap your phone or swipe a card. A cluster of neurons fires. A faint signal of discomfort registers. And for a fraction of a second, your brain genuinely reconsiders the purchase.

That friction is not a bug. It's a feature – one that's quietly disappearing as physical money becomes a relic of a pre-digital economy.

This article breaks down the neuroscience, behavioral economics, and practical psychology behind why cash feels different. More importantly, it explains how understanding that difference makes you a sharper, more deliberate spender – whether you carry a wallet full of bills or haven't touched paper money in years.

What Is 'Pain of Paying' – and Why It Matters

The core finding is simple: spending money hurts, and cash hurts the most. This isn't metaphor. Neuroimaging studies show that financial transactions activate the same brain regions associated with physical discomfort. The more tangible the payment method, the stronger the signal.

Behavioral economists call this the pain of paying – the psychological discomfort that accompanies any act of spending. Its intensity varies dramatically depending on how the payment is made.

Prelec & Loewenstein Study: Origin of the Concept

The foundational academic work on this concept comes from Drazen Prelec and George Loewenstein's 1998 paper, "The Red and the Black: Mental Accounting of Savings and Debt," published in Marketing Science (Vol. 17, No. 1, pp. 4–28.)

The paper introduced the concept of coupling – the degree to which the act of payment is psychologically linked to the act of consumption. Their central argument: when payment and consumption are tightly coupled (as with cash), the pain of paying acts as a natural brake on spending. When they're decoupled (as with credit cards or BNPL services), that brake weakens significantly.

Prelec and Loewenstein also demonstrated asymmetric loss aversion in financial decisions: the psychological weight of debt ("being in the red") outpaces the equivalent pleasure of savings ("being in the black"). This asymmetry explains why consumers often rush to pay off debt even when investing that money would be mathematically superior – a pattern I've seen play out repeatedly when working through household budget reviews with clients.

Why Cash 'Hurts' More Than Card

The mechanism is both psychological and neurological. Physical cash creates what researchers call payment salience – the vividness of the financial loss. When you hand over bills, the transaction is immediate, visible, and irreversible. The money leaves your hand. The wallet feels lighter. The stack is smaller.

A classic MIT experiment by Prelec and Simester put this to a direct test: participants bidding on NBA and MLB tickets were willing to pay 50–113% more when using a credit card compared to cash. For Boston Celtics tickets, the card-payment premium reached 113%. For Red Sox tickets, 76%. The payment method alone – not the buyer's income or the ticket's actual value – drove that gap. (Wired)

In a 2019 fMRI study published in Frontiers in Neuroscience ("Cash, Card or Smartphone: The Neural Correlates of Payment"), participants who observed cash payment scenarios showed significantly greater activation in the right inferior parietal cortex (BA40), the insula, and the posterior cingulate cortex (PCC) compared to card or smartphone payment scenarios – particularly at higher amounts ($150 vs. $10). The authors concluded:

"Payment by cash seems to be perceived by human brain as a significantly more salient stimulus than payment by card or smartphone." – Frontiers in Neuroscience, 2019 (PMC/NIH)

Card payments don't eliminate the pain – they delay and dilute it. By the time the credit card bill arrives, the connection between the discomfort and the specific purchase has dissolved. You feel vaguely worse about your finances, but you can't trace it back to the $34 dinner or the $12 subscription you forgot to cancel.

Neuroscience of Tangibility: Brain Dynamics in Cash Transactions

Cash activates a fundamentally different neural circuit than digital payment. Understanding which brain regions fire – and why – explains the behavioral differences that show up in spending data.

Insula Activation: Neural Trace of Physical Loss

The key player is the insula (or insular cortex), a region associated with processing negative emotions, physical discomfort, and visceral awareness. When you perceive a price as too high, the insula fires. When that activation is strong enough, it overrides the reward signal from the purchase – and you walk away.

Brian Knutson and colleagues documented this mechanism directly in a 2007 fMRI study published in Neuron ("Neural Predictors of Purchases," PMC). Participants made real purchasing decisions inside an MRI scanner. The findings were precise: insula activation in response to price negatively predicted purchase likelihood. The higher the insula response, the more likely the participant was to decline the purchase.

A Carnegie Mellon University summary of Loewenstein's related work captured it plainly:

"Credit cards effectively anesthetize the pain of paying… You swipe the card and it doesn't feel like you're giving anything up… unlike paying cash where you have to hand over bills." – Carnegie Mellon University (CMU)

Two regions work in dynamic tension during every purchase decision:

| Brain Region | Function | Activation: Cash vs. Card |

|---|---|---|

| Insula (Insular Cortex) | Processes negative emotions, physical discomfort, aversive stimuli | Significantly higher during cash payment, especially at larger amounts |

| Anterior Cingulate Cortex (ACC) | Monitors cognitive conflict, evaluates losses vs. gains | Elevated during cash transactions; reflects more complex decision-making |

| Posterior Cingulate Cortex (PCC) | Self-referential processing, sense of personal wealth | Activated during cash payment; encodes subjective sense of "my money leaving" |

| Inferior Parietal Cortex (BA40) | Calculates magnitude of wealth reduction, motor planning for handing over bills | Strongly activated during cash; scales with payment amount (p < 0.005) |

| Nucleus Accumbens (NAcc) | Reward anticipation, desire to acquire | Activated by desirable products; suppressed when insula response dominates |

Source: Frontiers in Neuroscience, 2019; Knutson et al., Neuron, 2007

Visualization of Expenses and Purchase Decision Impact

Cash doesn't just hurt more – it shows more. The physical act of paying makes the expense visible in a way that a card swipe never does. You watch the stack diminish. You count what's left. The budget becomes tangible.

A 2023 SSRN working paper, "Tapping Out: The Effect of Contactless Payments on Expenditure Recall" (SSRN), tested this directly. Participants assigned to contactless card payments showed significantly worse recall of their spending compared to those who paid with cash or PIN-verified debit cards. The cash group's recall errors hovered around 3–5%. The contactless group's errors ran 23–28% higher.

The practical implication is direct: if you can't remember what you spent, you can't manage it. Cash creates a running mental ledger that digital payments don't. Surveys from 2024–2025 reinforce this – roughly 30% of consumers acknowledge spending more when using contactless or digital payment methods, attributing it directly to reduced awareness of each transaction. The physical absence of money creates a psychological blind spot that shows up in the data every time.

Mental Accounting: Different Perceptions of 'Same' Money

Not all dollars feel equal – even when they're worth exactly the same. This is the central insight of mental accounting, and it explains behaviors that standard economics struggles to model.

Richard Thaler's Theory and Its Application to Cash

Nobel laureate Richard Thaler formalized this observation into a theory. His framework describes how people mentally segregate money into separate, non-fungible categories – and make decisions based on which "account" the money comes from, not its objective value.

"The main lesson to be learned from mental accounting… is that not all dollars are created equal." – Richard Thaler, Misbehaving: The Making of Behavioral Economics (2015)

Applied to cash, the theory reveals something counterintuitive. Physical bills often get mentally coded as "spending money" – the category for day-to-day, low-stakes transactions. Bank account balances, by contrast, feel more abstract and more "serious." This coding difference means that spending a $20 bill on an impulse purchase feels categorically different from spending $20 via card, even though the financial impact is identical.

In our experience reviewing household budgets, this pattern surfaces consistently. People who carry cash for groceries often overspend on snacks and convenience items – not because cash is less controlled, but because they've mentally labeled their wallet money as "already spent" before they even leave the house. The envelope system addresses this directly by assigning each cash allocation a specific purpose, which the practical section below covers in detail.

For a deeper look at how classic money management psychology interacts with these mental accounting effects, the classic money management psychology behind envelope budgeting is worth exploring.

Why 'Windfall' Money Is Spent More Easily

Mental accounting also explains the windfall effect – the well-documented tendency to spend unexpected money faster and more freely than earned income.

Earned wages arrive in the "serious money" account: rent, bills, groceries. A tax refund, a bonus, or a gift lands in a different mental bucket – one with fewer psychological restrictions attached. The money didn't come from labor, so it doesn't carry the same weight.

Harold Arkes and colleagues demonstrated this experimentally in 1994. Participants who received an unexpected cash windfall were significantly more likely to spend it on discretionary pleasures (like sporting event tickets) than participants who received the same amount as part of their regular income.

Nicholas Epley, Uri Gneezy, and Thomas Gilovich extended this in 2004: the less expected the income, the higher the probability of immediate hedonic spending. The mental category assignment happens automatically – and it drives behavior before any conscious deliberation occurs.

The practical risk is real. A $1,200 tax refund spent on a weekend trip represents the same financial impact as $100/month for a year. But it doesn't feel that way. And that feeling drives the decision.

Cash vs. Card vs. Digital Payments: Psychological Impact Comparison

The payment method is not neutral. Each step away from physical cash reduces the psychological friction that naturally limits spending. The data on this is consistent across decades of research.

Studies: How Much More Do We Spend With Cards?

| Payment Method | Average Spending Increase vs. Cash | Key Mechanism | Primary Research Basis |

|---|---|---|---|

| Cash | Baseline (0%) | Maximum pain of paying; physical loss is immediate and visible | Prelec & Simester (2001); Knutson et al. (2007) |

| Debit Card (PIN) | +10–15% | Reduced tactile loss; slight delay in perceived impact | SSRN "Tapping Out" (2023) |

| Credit Card | +12–30% (up to 113% in auction settings) | Decoupling of consumption and payment; reward network amplification | MIT/Prelec & Simester; Scientific Reports (2021) |

| Contactless / NFC (Tap-to-Pay) | +30–40% | Frictionless transaction; minimal cognitive engagement | Frontiers in Neuroscience (2019); SSRN (2023) |

| Mobile Wallet (Apple Pay / Google Pay) | +30–40% | Same as contactless, plus habitual automation | Behavioral FinTech reviews, 2024–2025 |

| BNPL (Klarna, Afterpay) | +40–60% | Full cost masked by installment framing; "deferral" of pain | Regulatory reports, 2024 |

| Cryptocurrency | Highest abstraction; quantification difficult | Casino-effect framing; volatility detaches value perception | Behavioral analogy from credit card fMRI data |

Sources: Prelec & Simester (2001); Scientific Reports, 2021 (Nature); SSRN, 2023; MIT Sloan, 2021 (MIT Sloan)

Digital Wallets, BNPL, and Cryptocurrency: Maximum Abstraction

Each layer of digital payment adds abstraction – and abstraction reduces the pain signal.

Digital wallets (Apple Pay, Google Pay) reduce transaction friction to a single gesture. The 2019 Frontiers in Neuroscience fMRI study showed that smartphone payment scenarios generated the weakest activation in pain-associated brain regions compared to both cash and card. Behavioral data from 2024–2025 reviews estimates a 10–25% increase in spontaneous purchase frequency compared to physical card use.

BNPL services (Klarna, Afterpay) exploit a more sophisticated mechanism: installment framing. When a $240 purchase becomes "four payments of $60," the full cost never registers as a single loss event. Regulatory reports through 2024 documented a 40–50% increase in user debt levels among BNPL adopters – a direct consequence of weakened financial self-control at the point of purchase.

Cryptocurrency operates at the furthest end of the abstraction spectrum. Without physical form, stable value, or cultural anchoring to "real money," crypto transactions activate what behavioral researchers describe as a casino-effect frame. Users treat digital assets as speculative chips rather than money, which dramatically lowers the psychological cost of loss. MIT Sloan research on credit cards noted that card purchases activate the same dopaminergic reward networks as addictive stimuli – crypto interfaces, with their price tickers, gain/loss animations, and gamified dashboards, amplify that effect further. (MIT Sloan)

For a detailed comparison of how these psychological dynamics play out in budgeting tools, the psychological impact of digital payments is worth reading alongside this piece.

Comparative Table: Tangibility and 'Pain' by Payment Types

| Payment Method | Tangibility Level | Pain of Paying Intensity | Expenditure Recall Accuracy | Impulse Purchase Risk |

|---|---|---|---|---|

| Cash | High | High | High (error: 3–5%) | Low |

| Debit Card (PIN) | Medium | Medium | Medium | Medium |

| Credit Card | Low | Low | Low | High |

| Contactless / Mobile | Very Low | Very Low | Low (error: 23–28% higher than cash) | Very High |

| BNPL | Near Zero | Near Zero | Very Low | Very High |

| Cryptocurrency | Zero | Near Zero | Very Low | Extreme |

Cognitive Biases Related to Physical Money

The psychology of cash isn't just about pain. Several distinct cognitive biases shape how physical money is perceived, valued, and spent – independent of the pain-of-paying mechanism.

Tangibility Effect

The tangibility effect describes a consistent cognitive pattern: people assign higher subjective value to physical money than to its digital equivalent, and part with it more reluctantly.

The operational definition: when the same financial loss is represented physically (bills leaving a hand) versus digitally (numbers decreasing on a screen), the physical version registers as more significant – even when the amounts are identical.

The Prelec and Simester experiment at MIT is the most-cited demonstration. Students paid up to twice as much for the same items when using a credit card compared to cash. The payment method – not the item's value, not the buyer's budget – drove the difference. (Wired)

In everyday financial behavior, the tangibility effect surfaces as:

- Stronger hesitation before cash purchases than equivalent card purchases

- More accurate post-purchase recall of cash spending amounts

- Greater effectiveness of cash-based budgeting systems (like envelope budgeting) compared to digital-only tracking

Anchoring: Valuing Through Physical Volume

The denomination effect is one of the most reliably replicated findings in cash psychology. The core result: people are significantly less willing to spend a single large bill than the equivalent amount in smaller denominations.

Helen Colby's working paper "Don't Break the $100 Bill: Large Bills Promote Savings" (Bayes Business School) frames it precisely:

"Large bills represent a partition that decision makers are reluctant to cross. When this partition is breached, discretionary spending is increased." – Helen Colby, "Don't Break the $100 Bill: Large Bills Promote Savings"

The mechanism is loss aversion applied to denomination: a $100 bill feels like a single, whole unit of value. Spending $15 from it means "breaking" something intact – and that psychological cost suppresses the purchase. Five $20 bills don't carry the same barrier. Each one is already a discrete, expendable unit.

A secondary effect compounds this: the denomination-spending matching effect. People unconsciously pair bill size to purchase size. A large bill feels appropriate for a large purchase, and inappropriate for a small one. This creates a natural spending filter – one that disappears entirely with card or mobile payment. Research published in the Journal of Consumer Research (2021) confirmed this matching behavior across multiple experimental settings, finding that denomination fit increased purchase satisfaction and reduced post-purchase regret.

Why We Underestimate Card Spending: The 'Blind Spot' Effect

The blind spot isn't a metaphor. It's a measurable gap between actual card spending and perceived card spending – and it runs consistently in one direction.

The 2023 SSRN paper "Tapping Out" (SSRN) quantified this directly. Contactless card users recalled their spending with 23–28% less accuracy than cash users. Cash users' recall errors stayed in the 3–5% range. The researchers noted a critical detail: subjective "pain of paying" ratings didn't differ between payment methods on self-report scales. The blind spot operates below conscious awareness.

This has direct practical consequences. Tracking spending with a card and relying on memory means working with systematically corrupted data. The problem isn't arithmetic – it's that the payment method neurologically reduces the salience of each transaction. The cognitive biases in budgeting that emerge from this blind spot are worth understanding before building any budget system.

Practical Implications: Using Cash Psychology in Personal Finance

The research converges on a clear practical direction. Cash's psychological properties – its pain signal, its tangibility, its denomination anchoring – can be deliberately deployed to improve financial self-control. Three techniques have the strongest evidence base.

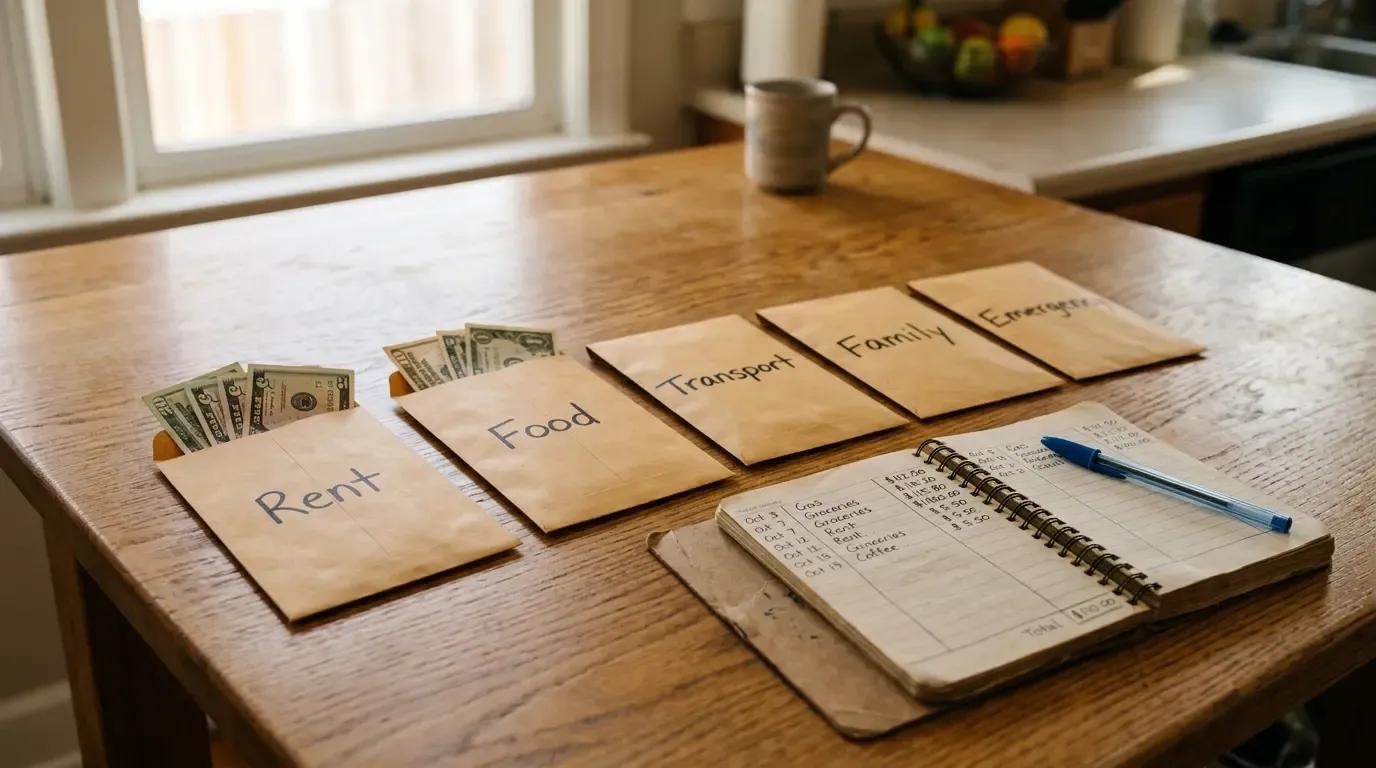

Envelope Budgeting: Structure and Effectiveness

Envelope budgeting translates mental accounting theory into a physical system. The structure is straightforward: after receiving income, allocate cash into labeled envelopes by spending category (groceries, dining, entertainment, transportation). When an envelope is empty, spending in that category stops until the next allocation period.

The system works because it operationalizes three psychological mechanisms simultaneously:

- Pain of paying – cash transactions activate the insula; each purchase costs something tangible

- Partitioning – envelopes function as hard mental accounting boundaries; "borrowing" from another envelope requires a conscious violation of the system's rules

- Denomination effect – using larger bills inside envelopes creates additional friction against small, impulsive purchases

The effectiveness data is consistent. According to surveys of financial advisors, up to 78% of people who consistently use envelope budgeting report meaningful improvement in financial control and debt reduction within the first year. Users of the method save approximately 10–15% more than comparable non-users.

Modern digital adaptations – YNAB (You Need A Budget) and Goodbudget – replicate the category structure virtually, assigning income to spending buckets before transactions occur. They don't fully replicate the neurological pain signal of physical cash, but they preserve the mental accounting architecture that makes the system effective.

For a complete walkthrough of how to implement this system, including category structures and allocation strategies, see the sustainable family budgeting guide.

Cash Diet: Temporary Return to Cash for Spending Correction

A cash diet is a time-limited behavioral intervention: switch entirely to cash for all discretionary spending for a defined period, typically 7 to 30 days. The mechanism is the pain of paying, deliberately reactivated.

The recommended duration depends on the goal. A one-week cash diet surfaces spending patterns and creates immediate awareness. A 30-day period is considered optimal for behavioral recalibration – long enough to disrupt ingrained card habits and establish new mental reference points for what spending "feels like."

Typical outcomes from documented cash diet periods include:

- 15–30% reduction in discretionary spending during the diet period

- Stronger adherence to pre-set budgets

- Improved awareness of spending category distribution

- Surplus funds available for debt repayment or savings

The effect is partly temporary – spending patterns often drift back toward baseline after returning to cards. But the awareness gained tends to persist. Clients who've completed a 30-day cash diet typically return with a much clearer picture of where their money was actually going, which makes every subsequent budgeting conversation more productive.

Hybrid Approach: Cash for 'Vulnerable' Spending Categories

A full-time cash diet isn't practical for most people in 2026. A hybrid model captures most of the psychological benefit without the operational friction.

The logic: identify the spending categories where impulse purchases are most likely – dining out, entertainment, personal care, online shopping – and fund those categories with cash. Use cards for planned, fixed, and low-risk categories: utilities, subscriptions, travel booked in advance.

This allocation strategy is directly supported by the research. The pain-of-paying effect is most protective in exactly the categories where impulsive decisions are most costly. Paying for a restaurant meal with cash activates the insula at the moment of decision. Paying a utility bill with autopay removes cognitive load from a transaction that offers no benefit from deliberation.

For people managing tight budgets or working to reduce debt, the organizing finances for mental clarity framework pairs well with this hybrid cash approach. If you want to model how different allocation splits affect your debt payoff timeline, the debt payoff calculator can help you run those numbers before committing to a category structure.

Cash Psychology in the Modern World: Cashless Society and Its Risks

The trend is clear and accelerating. Physical money is being displaced by digital infrastructure at a pace that behavioral economists are only beginning to fully study. The psychological consequences of that displacement deserve serious attention.

Trend Against Cash: Statistics and Forecasts

As of early 2026, cashless transactions account for over 70% of global payment volume, with projections placing that figure at 75% by year-end. The regional distribution is uneven:

- Scandinavia and South Korea: cashless share exceeds 95%

- Europe and North America: stabilized at 80–85%

- Emerging markets: rapid growth driven by mobile payment infrastructure

Visa and Mastercard's 2024–2025 annual reports documented explosive growth in tokenized and cross-border payments. McKinsey and the Bank for International Settlements (BIS) project that Real-Time Payment (RTP) systems and Central Bank Digital Currency (CBDC) pilots – particularly in Asia – will be the primary drivers through 2027.

A 2025 national survey in the United States produced a finding that cuts against the conventional narrative: only 30% of Gen Z respondents favor a fully cashless society. Seventy percent would not prefer complete elimination of cash – despite being the most digitally native generation in history. Among Boomers (60+), support for a cashless society was even lower. (FintechFutures, 2025)

Psychological Risks of a Completely Cashless Society

The research literature on cashless risk has grown substantially since 2020. Three categories of risk appear consistently.

Weakened financial self-control at the population level. The Journal of Consumer Psychology (2023) documented that the weakening of pain-of-paying through digital payments correlates with increased impulsive spending and rising personal debt levels. When the neurological brake is removed from every transaction, aggregate overspending increases – not just for individuals, but across demographic groups.

Digital exclusion and financial vulnerability. A 2024 World Bank report identified elderly individuals, low-income households, and residents of rural or underserved areas as disproportionately harmed by cashless infrastructure transitions. When cash is no longer accepted, these groups face material barriers to basic economic participation – not a psychological inconvenience, but an access problem.

Surveillance risk and loss of financial autonomy. The European Data Protection Board's 2025 report flagged total transaction trackability as a structural privacy concern. Every cashless payment generates a data point. Aggregated at scale, that data creates a comprehensive behavioral profile – one that can be used for commercial targeting, credit assessment, or, in more authoritarian contexts, social control. Cash's anonymity is not a bug. For a meaningful portion of the population, it's a feature.

For people navigating these tradeoffs while building financial independence without relying on credit infrastructure, the tangible budgeting for financial independence framework addresses how physical money management fits into a broader strategy.

Maintaining 'Reality' Sense of Money in the Digital Era

The pain of paying doesn't have to disappear just because physical cash does. Behavioral economists have identified several techniques that partially reconstruct the psychological friction of cash in digital environments.

Contextual velocity notifications. Standard transaction alerts have minimal impact on behavior. However, velocity notifications – alerts framed as "You've spent 80% of your weekly dining budget" rather than "Transaction: $14.50 at Chipotle" – reduce spending in the targeted category by 7–9%, according to 2024–2025 behavioral research.

Digital envelope visualization. Apps that visually deplete a budget "envelope" in real time – showing the remaining balance shrink with each purchase – reduce impulse purchase frequency by approximately 11% compared to standard transaction tracking. The visual depletion mimics the psychological experience of watching cash leave a wallet.

Deliberate friction at point of purchase. Requiring one additional confirmation step before completing a BNPL or high-value purchase – specifically one that displays the full total cost – reduces purchase completion rates by 9%. The pause forces conscious engagement with the full financial commitment.

The Bromoney Budget Planner app (iOS / Android) incorporates envelope-style visual budgeting alongside spending velocity alerts – designed to recreate the psychological salience of cash management in a fully digital workflow.

Frequently Asked Questions (FAQ)

Why Is It Psychologically Harder to Spend Cash?

Spending cash is harder because it activates the brain's pain-processing regions – specifically the insula and anterior cingulate cortex – in a way that card and digital payments do not. The physical act of handing over bills makes the loss immediate, visible, and irreversible. There's no decoupling between the moment of consumption and the moment of payment. The brain registers the transaction as a real reduction in personal resources, which creates genuine psychological resistance to the purchase.

Do People Really Spend More With Cards?

Yes, and the magnitude is substantial. The MIT experiment by Prelec and Simester found that participants bid 50–113% more for the same items when paying by credit card compared to cash. A 2021 Scientific Reports fMRI study (Nature) identified the neurological mechanism: credit card purchases strongly activate the brain's reward network (striatum) regardless of price, while cash purchases show reward activation that diminishes as price increases. The card doesn't just reduce pain – it amplifies the pleasure of buying.

What Is Mental Accounting and Its Connection to Cash?

Mental accounting, developed by Richard Thaler, describes the cognitive process by which people mentally categorize money into separate, non-interchangeable accounts – "vacation fund," "grocery money," "pocket cash." Physical cash reinforces this categorization because its tangibility makes each bill feel purpose-specific. Bills in a wallet feel like "spending money." Funds in a bank account feel like "serious money." This categorical separation means that spending cash on an impulse purchase triggers less psychological resistance than spending the same amount via card, because the mental account is already coded for expenditure.

Does Envelope Budgeting Help Save Money?

The evidence says yes. Up to 78% of consistent envelope budgeting users report significant improvement in financial control and debt reduction within the first year, according to financial advisor surveys. Average savings rates improve by 10–15% compared to non-users. The system works through three reinforcing mechanisms: the pain of paying (cash transactions register as real loss), partitioning (envelope boundaries create hard mental accounting limits), and denomination anchoring (larger bills inside envelopes add friction against small purchases). Digital adaptations like YNAB preserve the mental accounting architecture even without physical cash.

How Does Pain of Paying Work in the Age of Apple Pay and Google Pay?

It largely doesn't – and that's the problem. The 2019 Frontiers in Neuroscience fMRI study showed that smartphone payment scenarios generated the weakest brain activation in pain-associated regions of any payment method tested. The frictionless, single-gesture nature of mobile payments reduces the transaction to a near-unconscious act. The 2023 SSRN study "Tapping Out" confirmed that contactless payment users recall their spending with 23–28% less accuracy than cash users – even though their self-reported "pain of paying" scores were similar. The pain is there, but it's too faint to influence behavior. Practical countermeasures – velocity alerts, digital envelope visualization, deliberate confirmation steps – can partially restore that friction, but they require intentional setup.

Denis Goncharenko

Managing Editor & FinTech Content Strategist

Editorial Policy: Denis ensures every financial claim is backed by institutional data sources.

Was this article helpful?

Same blogs

Cash Stuffing for Undocumented Workers: A Complete Guide to Budgeting Without a Credit History

No SSN, no credit history, no bank account – the envelope budgeting method gives undocumented workers full control over their cash income. This guide covers every practical step, from setting up your first envelopes to building toward long-term financial stability.

Refinancing vs Debt Consolidation: What These Terms Actually Mean

Learn the real difference between refinancing and debt consolidation to choose the right strategy for your financial situation.

The Envelope Method's Hidden Traps: When Your Budget Creates a False Sense of Financial Security

The envelope method feels like control. But in reviewing household budgets, the same pattern keeps appearing: people who follow their envelopes religiously and still end up in financial crisis. Here's why the envelopes were full while the financial picture was not.