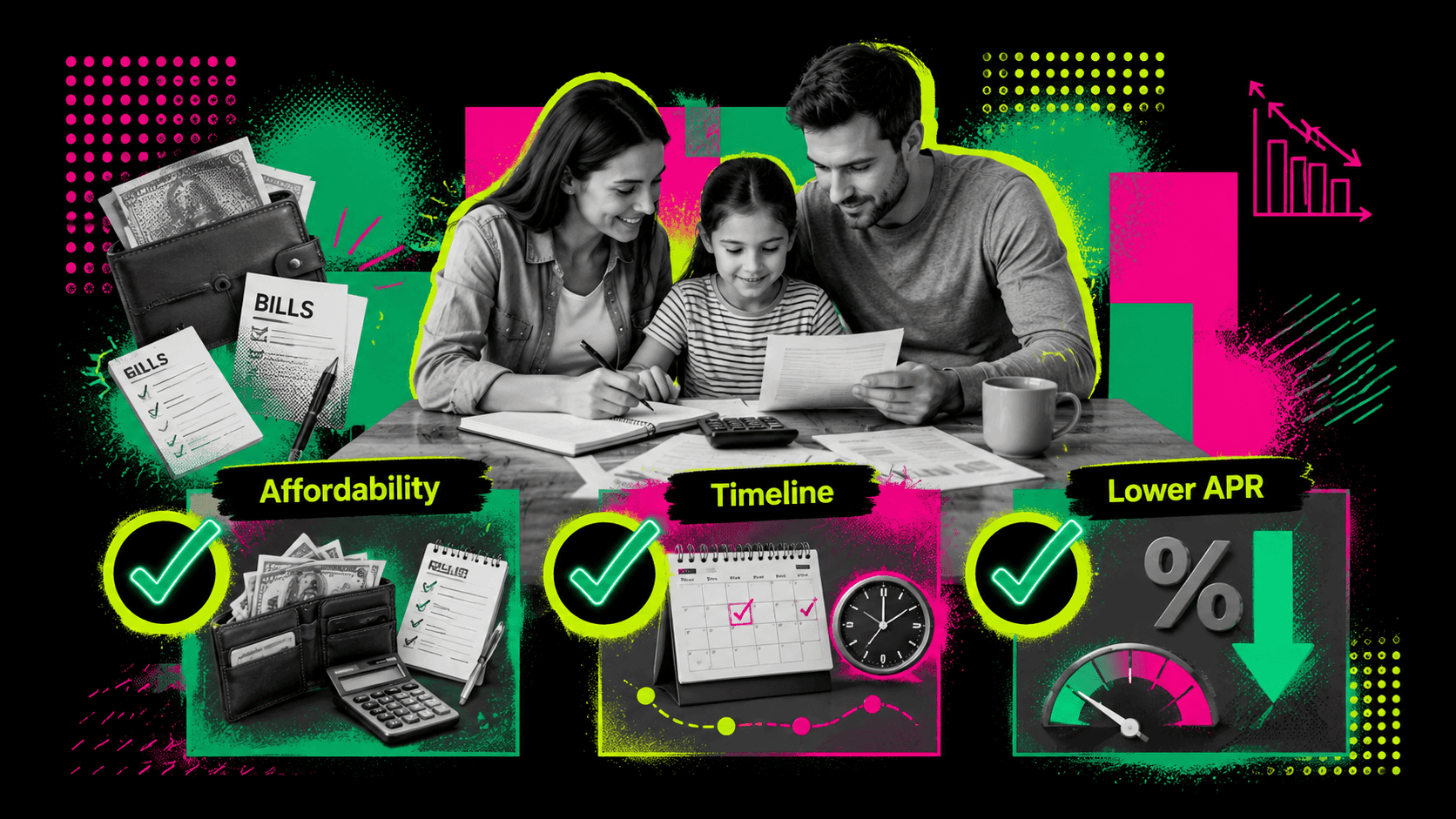

Debt Consolidation Quick Self-Check: Affordability, Timeline, Lower APR

A debt consolidation offer can look helpful before the borrower checks the numbers. One payment sounds easier than five. A lower monthly payment feels like relief. A lender page may show a clean estimate in seconds. Yet the real question is not only whether a borrower can get approved, but also whether the new loan makes the debt cheaper, clearer, and easier to finish.

That is where a quick self-check helps. Before using a debt consolidation calculator or applying for a loan, the borrower should test three things: affordability, timeline, and lower APR. If the new payment fits the budget, the payoff date makes sense, and the APR improves after fees, consolidation may deserve a closer look. If one of those pieces fails, the offer needs caution.

Debt consolidation is not a magic discount. It usually moves existing balances into a new structure. The benefit comes from better terms, fewer due dates, and a repayment plan that actually reaches zero. The cost comes from interest, fees, possible credit impact, and the risk of building new balances after old ones are paid.

Why the Self-Check Comes Before the Application

Many borrowers start with approval, which is understandable. Debt pressure makes any "you qualify" message feel useful. But approval is not the same as improvement. A borrower can qualify for a loan that costs more than the current debt, stretches repayment longer than necessary, or creates a lower payment by adding years of interest.

The Consumer Financial Protection Bureau warns borrowers to review important details before consolidating credit card debt, including rates, fees, promotional terms, and whether spending behavior will change after payoff. That advice matters because debt consolidation usually succeeds or fails after the old balances are cleared. If paid-off cards start carrying balances again, the borrower has not solved the debt problem. The borrower has duplicated it.

A self-check creates a pause before a hard credit inquiry, origination fee, or new loan agreement. It helps the borrower separate emotional relief from financial improvement. The process does not need to be complicated. It needs accurate balances, current APRs, realistic monthly cash flow, and a full view of fees.

What a Debt Consolidation Calculator Should Show

A debt consolidation calculator should do more than estimate a monthly payment. A useful calculator compares the current debt path with the proposed consolidation path. It should show current balances, interest rates, minimum payments, expected payoff time, total interest, new loan APR, loan term, fees, new monthly payment, and total repayment cost.

A basic payment estimate is not enough because a lower payment can come from a longer term. That can help short-term affordability, but it may increase the total amount paid. A borrower who only looks at the monthly number may choose the offer that feels easiest while missing the offer that saves more money.

A debt consolidation loan calculator should also account for origination fees. If a lender charges a fee and deducts it from the loan proceeds, the borrower may receive less money than expected. That matters when the goal is to pay creditors in full. A $15,000 loan with a 5% origination fee may deliver $14,250 before creditor payments. The missing $750 still has to come from somewhere.

A strong debt consolidation payment calculator also lets the borrower test different terms. A 36-month term, 48-month term, and 60-month term can produce different monthly payments and different total costs. The right choice is not automatically the shortest or longest term. The right choice is the term that fits the budget while keeping the total cost reasonable.

Self-Check #1: Affordability

Affordability starts with cash flow, not with lender approval. The borrower should know how much money remains after housing, utilities, food, transportation, insurance, minimum debt payments, and irregular expenses. Irregular expenses matter because they are the bills that usually push people back to credit cards: car repairs, medical copays, annual subscriptions, school costs, pet care, and travel obligations.

A debt consolidation loan payment calculator can estimate the new payment, but the borrower has to test that number against real life. A payment that fits only in a perfect month does not fit. A useful payment should survive a normal, messy month without forcing new credit card use.

This is where many consolidation plans break. The loan pays off old cards, the new payment starts, and the budget has no room for emergencies. Then one unexpected expense goes back onto a card. The consolidation loan remains, and a new card balance appears.

A safer affordability test includes a small monthly buffer. The buffer does not need to be large, but it needs to exist. If the proposed loan payment uses every available dollar, the borrower should look at a different term, a lower loan amount, a nonprofit credit counseling plan, or a broader budget reset before signing.

Self-Check #2: Timeline

The payoff timeline tells the truth about the loan. A debt consolidation loan can lower the monthly payment, but it may still be a poor deal if it prolongs the borrower's debt much longer. The goal is not only to breathe this month. The goal is to create a route to zero.

A timeline check compares the current payoff path with the proposed loan term. If the borrower continues to pay the current minimums, the payoff date may be far away because credit card minimums decrease as balances are paid down. A fixed installment loan can improve that by creating a set end date. That is one reason personal loans can work well for credit card consolidation.

The term should match the borrower's financial capacity. A 36-month loan may save interest but create a payment that strains the budget. A 72-month loan may lower the payment, but keep debt alive for six years. A middle term may work better if it protects cash flow and avoids excessive interest.

A debt consolidation loan calculator helps here because it turns the timeline into dollars. The borrower can see how much interest each term adds. That view prevents a common mistake: choosing the loan that has the lowest monthly payment without seeing the long-term cost.

The best timeline is clear, realistic, and shorter than drifting on minimum payments. If the proposed consolidation plan does not create a better payoff path, it needs a stronger reason to exist.

Self-Check #3: Lower APR

The APR check is the most obvious, but it is also the easiest to mishandle. A borrower should compare the new APR with the weighted average APR of the debts being consolidated. A simple average can mislead. A $10,000 balance at 24% matters more than a $500 balance at 15%.

The new loan does not need to beat every single existing rate, but it should improve the overall cost of the debts included in the plan. If a borrower includes low-interest debt in a higher-rate consolidation loan, the math gets worse. Not every debt belongs in the consolidation package.

Fees belong in this APR conversation. A loan with a lower rate but a large origination fee may cost more than expected. A balance transfer card with a 0% promotional APR may still carry a 3% to 5% transfer fee. A home equity loan may carry closing costs. A HELOC may start with a lower variable rate that changes later.

The cleanest approach is to compare total repayment cost, not just APR. APR is a useful signal. Total dollars paid is the final answer. If the new loan costs less, creates a clear payoff date, and fits the budget, the APR check passes.

How Much Is Debt Consolidation?

The question "how much is debt consolidation?" has no single answer because the cost of debt consolidation depends on the product. A personal loan may include interest and an origination fee. A balance transfer card may include a transfer fee and a promotional APR that expires. A home equity loan may include closing costs. A debt management plan may include setup or monthly fees through a credit counseling agency.

The cost also depends on the borrower's profile. Credit score, income, debt-to-income ratio, loan size, collateral, and repayment term all affect pricing. Two borrowers with the same debt balance can receive different offers because lenders see different risks.

The borrower should separate the three types of costs. Upfront cost is what gets charged at the start, such as origination fees, transfer fees, or closing costs. The monthly cost is the required payment. Lifetime cost is the total paid until the balance reaches zero.

Lifetime cost matters most. A loan with no upfront fee but a high APR may cost more than a loan with a small fee and a lower rate. A low payment may cost more if the term is long. A promotional card may cost less if the balance is paid before the promo ends and more if the regular APR takes over.

How Much Does Debt Consolidation Cost in Real Numbers?

A simple example shows why the calculator matters. Suppose a borrower has $18,000 in credit card debt at a weighted average APR of 24%. The current minimum payments total $540 per month. If the borrower takes a 48-month personal loan at 13% APR with a 3% origination fee, the monthly payment may be higher or lower than the current minimum depending on the exact fee treatment and lender terms. But the key comparison is total interest and payoff date.

If the current credit card plan relies on shrinking minimum payments, payoff can stretch for years and cost far more in interest. If the fixed loan payment retires the debt in 48 months, the borrower gains a clear endpoint. The origination fee still matters, but it may be worth paying if the total cost drops and the budget can handle the payment.

Now change the facts. If the borrower qualifies only for a 25% APR personal loan with a 6% origination fee, the consolidation loan may cost more than the cards. The payment may look organized, but the math fails. In that case, a nonprofit debt management plan, hardship program, or balance transfer may deserve review.

This is why "how much does debt consolidation cost" should be answered with a comparison, not a range. The cost is the difference between staying on the current path and accepting the new path.

Debt Consolidation Loan Payment Calculator

A calculator is only as useful as the numbers entered. The borrower should use current balances, not old statement balances. Credit card interest accrues daily, and recent purchases or pending payments can change the payoff amount. Using stale balances can leave residual debt after consolidation.

The borrower should enter APRs, not only interest rates from memory. The APR includes more of the borrowing cost and gives a cleaner comparison. For credit cards, the purchase APR may differ from the cash advance APR or promotional APR. The borrower should use the rate that applies to the balance being consolidated.

Minimum payments should also be current. Many credit card minimums change as balances change. If the calculator asks for the expected monthly payment on the current path, the borrower should decide whether to compare against minimums or against the amount currently being paid. That choice affects the result.

For the new loan, the borrower should enter the loan amount, APR, term, origination fee, funding method, and whether the fee is deducted from proceeds or added to the balance. If the lender pays creditors directly, the calculator should still account for any leftover balance caused by fees or interest accrual.

What a Good Result Looks Like

A good calculator result shows three things at once: the payment fits, the timeline is clear, and the total cost improves. The borrower should be able to say, "This loan pays these accounts, costs this much, ends on this date, and saves this amount compared with my current path."

A good result does not always mean the lowest monthly payment. Sometimes the better result has a slightly higher payment but a shorter term and less interest. Sometimes the better result is a longer term because it prevents missed payments and still lowers total cost. Context matters.

The plan should also include behavior controls. Paid-off cards need rules before the loan funds. The borrower may remove cards from digital wallets, set spending alerts, lower limits, freeze cards, or keep one card for a small recurring charge paid in full. Without a card rule, the calculator result becomes theoretical.

A good result also leaves room for emergencies. Debt consolidation should not make the budget so tight that the next surprise expense creates new debt.

When the Calculator Says "No"

Sometimes the calculator shows that consolidation does not help. That is useful information, not a failure. If the new APR is too high, the fees are too large, or the timeline is too long, the borrower has avoided a bad loan.

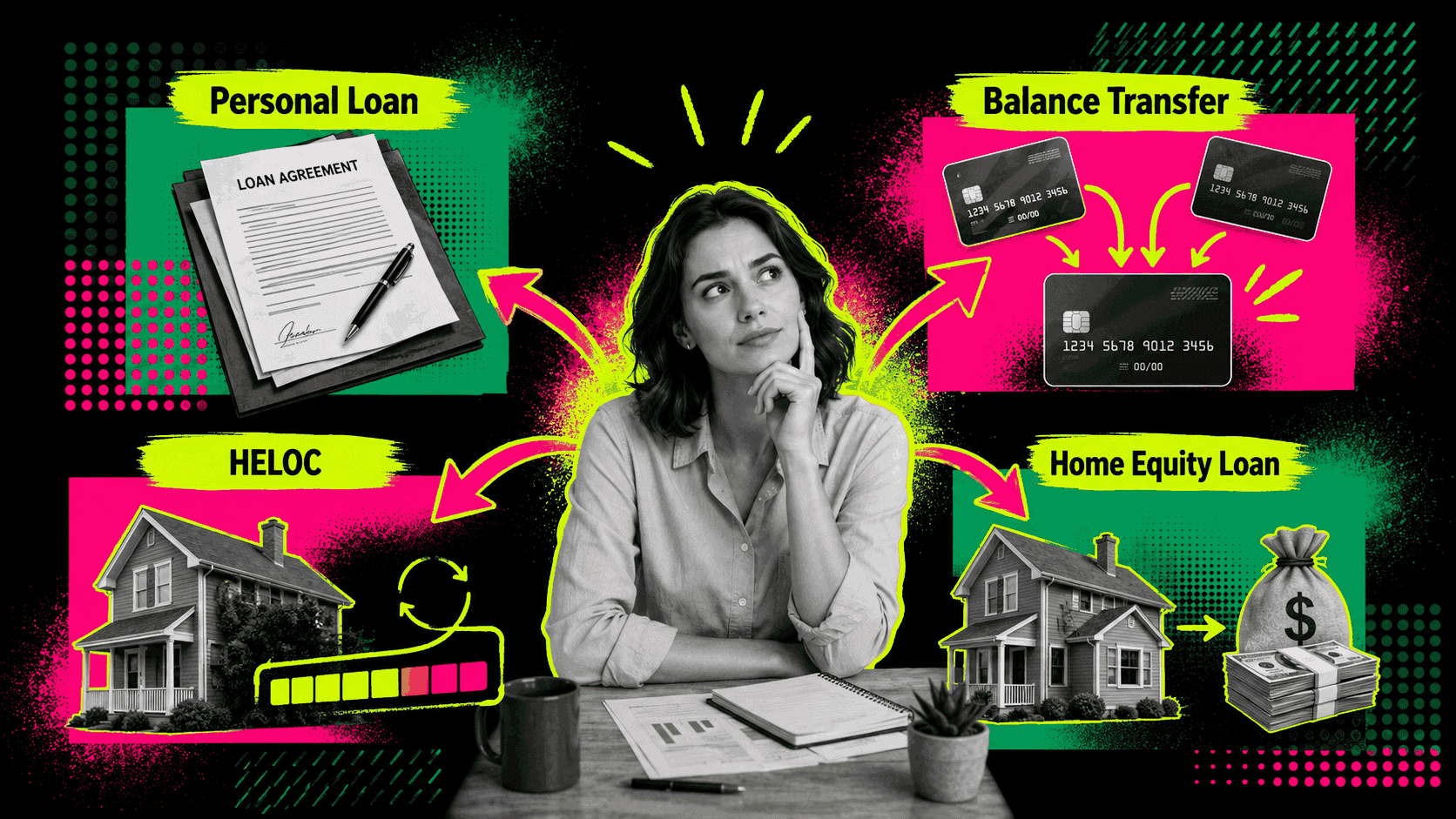

When the calculator says "no", the borrower can try a few safer adjustments. Exclude low-interest debts from the consolidation amount. Improve your credit before applying. Compare credit unions and online lenders. Consider a balance transfer if the payoff window is short. Speak with a nonprofit credit counseling agency about a debt management plan.

The borrower should be careful with companies that promise quick debt relief or guaranteed savings. The FTC says many debt relief companies covered by the Telemarketing Sales Rule cannot charge fees before they settle or otherwise resolve a consumer's debt. That rule exists because distressed borrowers are vulnerable to expensive promises.

A "no" from the calculator can also reveal a deeper issue. If no payment fits the budget, the problem may not be the interest rate. The problem may be income, expenses, or debt level. In that case, another loan may not be the right first move.

Common Calculator Mistakes

The first mistake is ignoring fees. A debt consolidation payment calculator that does not include origination fees, balance transfer fees, or closing costs gives an incomplete answer. Fees can turn a good-looking rate into a mediocre deal.

The second mistake is using the wrong comparison. If the borrower compares a new fixed loan payment with current credit card minimums, the loan may look expensive. If the borrower compares the total interest and the payoff date, the loan may look better. Both views matter.

The third mistake is consolidating every debt automatically. Low-interest debt may not belong in the plan. Federal student loans require extra caution because private refinancing can remove federal protections.

The fourth mistake is treating prequalification as final approval. Prequalification can help compare estimated rates, often through a soft credit check, but final terms can change after full underwriting.

The fifth mistake is forgetting post-payoff behavior. A calculator cannot predict whether paid-off cards will stay at zero. The borrower has to build that protection into the plan.

Final Takeaway

A debt consolidation calculator helps only when it answers the right questions. The borrower should not use it merely to ask, "What will my payment be?" The stronger questions are: "Can I afford this payment in a normal month? Does this timeline move the debt toward zero fast enough? Is the APR lower after fees? What is the full debt consolidation cost?"

Debt consolidation can be worth it when the math and the behavior plan work together. The new payment should fit. The payoff date should be clear. The total cost should improve. The borrower should know what happens to every paid-off account after the loan funds.

If the calculator shows savings but the budget has no room, the plan is fragile. If the payment fits but the loan costs more, the plan is expensive. If the numbers work, but the cards will be used again, the plan is incomplete. The best consolidation decision is not the one that creates the smallest payment. It is the one that creates a realistic route to zero.

Frequently Asked Questions

What is a debt consolidation calculator?

A debt consolidation calculator compares current debts with a proposed consolidation option. It can estimate the monthly payment, payoff timeline, interest cost, fees, and total repayment cost.

What is a debt consolidation loan calculator used for?

A debt consolidation loan calculator helps borrowers compare a new loan against existing debts. It should show whether the new APR, fees, term, and payment improve the current repayment path.

How much is debt consolidation?

Debt consolidation cost depends on the product, APR, fees, term, loan size, and borrower's credit profile. Personal loans may include origination fees. Balance transfers may include transfer fees. Home equity products may include closing costs.

How much does debt consolidation cost if there is no upfront fee?

Even without an upfront fee, debt consolidation still costs interest. The borrower should compare the total repayment cost, not only the monthly payment or advertised APR.

Is a debt consolidation payment calculator enough before applying?

No. A calculator gives the math, but the borrower also needs a budget check and a behavior plan. Paid-off cards should not become new debt after consolidation.

Denis Goncharenko

Managing Editor & FinTech Content Strategist

Editorial Policy: Denis ensures every financial claim is backed by institutional data sources.

Was this article helpful?

Same blogs

Debt Consolidation Options Compared: Which Path Fits Your Debt?

Compare debt consolidation options including personal loans, balance transfers, home equity, and debt management plans to find your best path.

Refinancing vs Debt Consolidation: What These Terms Actually Mean

Learn the real difference between refinancing and debt consolidation to choose the right strategy for your financial situation.

Compare: Personal Loan vs Balance Transfer vs HELOC vs Home Equity Loan

Compare four debt consolidation options to find the right balance between cost, risk, and flexibility for your situation.